Qantas delivered a solid but not spectacular first half, with underlying pretax profit rising 5.1% to A$1.46 billion, narrowly beating analyst expectations of A$1.43 billion. Revenue grew 6.3% to A$12.90 billion, though it fell just short of consensus. The headline numbers mask a more nuanced picture that retail investors should examine carefully.

The star performers were Jetstar and Qantas Loyalty, both posting 12% EBIT growth. Jetstar’s improvement was largely driven by new, fuel efficient Airbus aircraft, with management attributing around 60% of the division’s profit uplift to the newer fleet. Loyalty continues to be a high margin, capital light earnings engine, with full year EBIT growth guided at 10 to 12%. These two segments are increasingly important as the traditional airline operations face headwinds.

The concern lies in Qantas International, where EBIT fell 8.3% to A$300 million, well below the A$349 million estimate. Demand dynamics are shifting: while US to Australia bookings have strengthened, economy class travel from Australia to the US has weakened, forcing schedule adjustments. This is an early signal that the post pandemic travel boom may be normalising, particularly in discretionary long haul leisure travel.

Domestically, EBIT grew a modest 4.5% but also missed estimates. Qantas made the unusual move of scaling back planned domestic capacity growth after corporate travel demand came in softer than expected. For an airline that has enjoyed strong pricing power, this is worth watching.

Cash flow is the most striking red flag. Net free cash flow swung to negative A$57 million from positive A$677 million a year ago. This reflects the massive fleet renewal program, with capital expenditure guided at A$4.1 to A$4.3 billion this year and rising to A$5.1 to A$5.4 billion in FY27. While new aircraft will deliver long term fuel savings and revenue benefits, this investment cycle will pressure returns for several years.

Cost pressures are building too. Fuel costs rose 2.9% and came in above estimates, airport charges and government fees are increasing at double the rate of inflation, and the Same Job Same Pay legislation will add approximately A$95 million in costs this financial year.

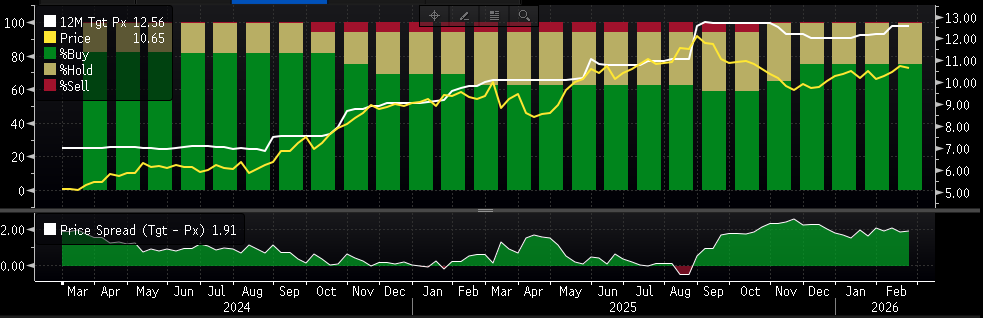

On the positive side, the 20% dividend increase and A$150 million buyback signal management confidence. The stock trades at A$10.65 against a consensus target of A$12.56, implying nearly 18% upside. With 75% buy ratings and zero sells, the market remains optimistic.

The bottom line: Qantas is navigating a tricky transition, investing heavily in its future while facing softening demand in key segments and rising costs. The earnings quality is decent but not accelerating, and the cash flow profile will test investor patience through FY27 and beyond.

The Bloomberg consensus chart (attached image) is the most useful visual for retail investors here. It shows 75% of analysts rating Qantas a Buy with a A$12.56 target price versus the current A$10.65, illustrating the market’s conviction that the stock is undervalued despite the operational headwinds discussed above. The narrowing price spread (target minus actual) over the past year also shows the stock has been steadily closing the gap to fair value, having rallied roughly 29% over the last twelve months. This context helps investors gauge whether the remaining upside adequately compensates for the fleet investment risks and demand softening outlined in the summary.