Evolution Mining is one of Australia's largest listed gold producers, operating five wholly owned mines across Australia and Canada - Cowal (NSW), Ernest Henry and Mt Rawdon (Queensland), Mungari (Western Australia), and Red Lake (Canada). The company also holds the Northparkes copper-gold operation, which has materially shifted its production profile and added meaningful copper exposure.

A Macro Backdrop That Keeps Working in Gold’s Favour

The setup for Australian gold producers heading into the second quarter of 2026 is difficult to fault. Escalating conflict in the Middle East has driven persistent safe-haven demand, pushing gold above US$4,400 per ounce and well above A$7,200 in Australian dollar terms. Central banks continue to accumulate, J.P. Morgan expects around 755 tonnes of official sector purchases this year, still elevated relative to the pre-2022 average of 400-500 tonnes. Meanwhile, the Australian dollar has weakened to around US$0.687, down from above US$0.72 in February, amplifying gold revenues for domestic producers.

Domestically, the RBA’s decision to raise the cash rate to 4.10% in March – its second consecutive hike, passed by a single vote – reflects an economy grappling with renewed inflationary pressures, partly driven by higher fuel costs tied to the Middle East conflict. For gold miners like Evolution, this macro cocktail of geopolitical risk, persistent inflation, and a softer Australian dollar translates directly into higher realised prices.

There is a counterweight, however. Brent crude has surged above US$105 per barrel, up roughly 35% year-to-date, and diesel is the lifeblood of open-pit mining operations. The industry rule of thumb is that every 10% rise in crude oil adds approximately 2% to all-in sustaining costs, implying a potential 7% uplift at current oil prices. For Evolution, that would push AISC toward the upper end of its $1,640-$1,760 per ounce guidance range. But with gold above A$7,200 per ounce, the margin buffer remains substantial. Larger producers like Evolution are also better positioned than juniors to manage fuel supply risk, given their scale and long-term procurement arrangements.

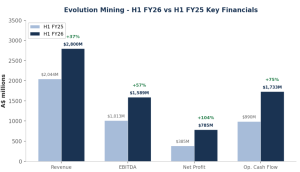

Record Earnings Confirm the Thesis

Evolution’s first-half FY26 results, released in February, showed the company capitalising on this environment. Statutory net profit hit a record $767 million for the six months to 31 December 2025, with underlying profit surging 104% to $785 million. Revenue climbed 37% to $2.8 billion. Operating mine cash flow reached $1,733 million, up 75%, while net mine cash flow of $1,093 million was up 151%. The balance sheet has been transformed – cash on hand rose 86% to $967 million, with gearing at just 6%. Shareholders were rewarded with a record fully franked interim dividend of 20 cents per share.

Source: Evolution Mining H1 FY26 Financial Results

RBC Capital recently upgraded Evolution to Sector Perform from Underperform, raising its price target to $14.50 from $9.90. The consensus fair value has been revised to $13.91, and at the current price around $12.40, the stock trades below both marks.

Analysis and Implications

Full-year FY26 guidance of 710,000 to 780,000 ounces of gold and 70,000 to 80,000 tonnes of copper at an all-in sustaining cost of $1,640 to $1,760 per ounce positions Evolution to generate substantial free cash flow while gold remains anywhere near current levels. The underlying EBITDA margin has expanded to 57%, up 14 percentage points, reflecting both the commodity price tailwind and disciplined cost management.

The Northparkes copper-gold asset adds diversification and leverage to copper’s own structural demand story via electrification and the energy transition. With nearly $1 billion in cash and minimal gearing, Evolution has flexibility for further shareholder returns, reinvestment, or opportunistic M&A – and the macro environment gives management room to be selective.

The Takeaway

Evolution Mining enters the March quarter reporting season (results due 15 April) with record earnings, a fortified balance sheet, and a macro backdrop that continues to favour gold. Geopolitical uncertainty, central bank buying, and a weaker Australian dollar are sustaining elevated gold prices in AUD terms. For investors with exposure to the Australian gold sector, EVN is well positioned as we approach the next operational update.