Fortescue Metals, the world’s fourth-largest iron ore producer and a common holding in client’s portfolios.

Fortescue’s March quarter results paint a mixed picture for investors. The iron ore miner shipped a record 148.7 million tonnes over the first nine months of FY26, up 4% on the same period last year. Quarterly shipments of 48.4 million tonnes were 5% above the prior year, though they fell 4% compared to the previous quarter.

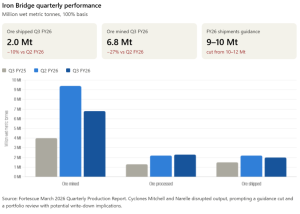

The standout concern remains Iron Bridge, the magnetite operation that produces a higher grade concentrate. Two tropical cyclones disrupted production, prompting the company to cut its FY26 Iron Bridge shipment guidance to 9 to 10 million tonnes, down from the previous 10 to 12 million tonnes. This is significant because Iron Bridge has consistently underdelivered since commissioning, and analysts at Jefferies have flagged the risk of an impairment charge at the full year results, citing the asset’s disappointing contribution. Jefferies maintains an underperform rating with a price target of A$16.50, well below the recent share price near A$19.78.

Pricing tells another important story. The standard hematite product realised US$92 per tonne, only 89% of the benchmark Platts 61% index. This discount reflects the lower grade of Fortescue’s mainstay products, with the lower quality Super Special Fines now making up 45% of shipments. By contrast, Iron Bridge concentrate fetched US$122 per tonne, a premium to benchmarks, which is precisely why its production shortfall hurts more.

On costs, the hematite C1 unit cost of US$18.29 per wet tonne improved 4% from the prior quarter, sitting within FY26 guidance. However, the cash balance fell to US$4.2 billion from US$4.7 billion three months earlier, and net debt rose to US$1.6 billion from US$1.0 billion, reflecting the US$1.3 billion interim dividend payment and US$915 million of capital expenditure.

Strategically, Fortescue continues to push hard into green energy and copper. It approved a US$680 million Pilbara green energy investment targeting data centre demand, completed the Alta Copper acquisition for about US$70 million, and expects first hot metal from its Christmas Creek green metal project in the June quarter.

The bigger issue for investors is the announced portfolio review of Pilbara operations, with an update due in three months. This effectively confirms management is rethinking Iron Bridge’s role, and a write-down looks increasingly possible.

Headline production records mask underlying weakness in pricing, rising debt, and an underperforming growth asset. The green strategy may pay off eventually, but it is consuming significant capital today while iron ore prices stay under pressure.