Resolute is an African-focused gold miner with more than 30 years of experience as an explorer, developer and operator.

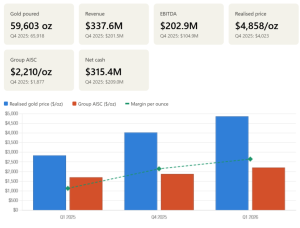

Resolute Mining delivered a financially robust March quarter, with the headline numbers flattered by record gold prices. The West African gold miner produced 59,603 ounces, down ten percent from Q4 2025, but generated $337.6 million in revenue and $202.9 million in EBITDA, both roughly double the prior quarter. This jump is almost entirely attributable to a 21 percent rise in the average realised gold price to $4,858 per ounce, combined with a 39 percent increase in ounces sold as inventory was drawn down.

The balance sheet was meaningfully strengthened. Operating cash flow of $119.8 million pushed the net cash position to $315.4 million, up from $209.0 million at the start of the year, with available liquidity of $425 million. This positions Resolute to fund the Doropo project in Côte d’Ivoire, where ground clearance has begun and first gold is targeted for the second half of 2028. Capital expenditure of $33.4 million was relatively light, with management flagging that 75 percent of Doropo’s $170 to $190 million 2026 budget is weighted to the second half.

Investors should look beyond the headline cash flows, however. Group all-in sustaining costs rose 18 percent quarter on quarter to $2,210 per ounce, with Syama hitting $2,227 per ounce against full-year guidance of $1,950 to $2,150. Royalty payments tied to higher gold prices added roughly $135 per ounce above the level assumed in guidance. Management has also warned that fuel prices, up around 50 percent in Mali and 30 percent in Senegal, could add a further $75 and $50 per ounce respectively if sustained. While production guidance of 250,000 to 275,000 ounces is maintained, the AISC range is explicitly subject to revision, suggesting cost guidance may be at risk.

Production is heavily weighted to the second half, dependent on successful commissioning of the Syama Sulphide Conversion Project in Q3, an execution risk worth monitoring. Geographic concentration in Mali, Senegal and Côte d’Ivoire also exposes the company to West African political and security risks, illustrated by the recent unrest in Bamako. The selected chart highlights the central investment story: margin per ounce has more than doubled in twelve months despite rising costs, but that cushion depends entirely on the gold price holding up.