Northern Star Resources Limited engages in the exploration, development, mining, and processing of gold deposits. The company also sells refined gold. It operates in Western Australia, the Northern Territory, and Alaska. Northern Star Resources Limited was incorporated in 2000 and is headquartered in Subiaco, Australia.

Northern Star Resources delivered an improved March 2026 quarter. The Australian gold miner sold 381koz at an all-in sustaining cost of A$2,709 per ounce, generating revenue of A$2,012 million and underlying free cash flow of A$301 million.

The standout positive was operational momentum across most sites. Thunderbox lifted sales 26 percent quarter-on-quarter on higher grades, better recoveries and first ore from the Bannockburn open pit. Pogo in Alaska improved grades through stope optimisation, cutting unit costs meaningfully. KCGM, the flagship Kalgoorlie operation, delivered higher grades from the Golden Pike North area, prioritising margin during current mill capacity constraints.

However, the quarter capped a series of guidance downgrades that warrant scrutiny. The company revised full-year production guidance lower in March to above 1,500koz, with KCGM sales now forecast at 450 to 480koz versus the prior 520 to 550koz. AISC guidance was lifted earlier in the year to A$2,600 to A$2,800 per ounce. The KCGM Mill Expansion capex was again revised upward, citing poor construction productivity and cost inflation, with FY26 spend now A$680 to A$700 million and FY27 lifted to roughly A$160 million.

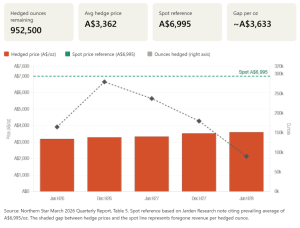

A critical issue for shareholders is the realised gold price of A$5,283 per ounce, roughly 24 percent below the prevailing spot average of around A$6,995 per ounce. Legacy hedges delivered at A$3,168 per ounce dragged the average lower, and 953koz remain hedged at A$3,362 per ounce through to mid-2028. Investors are therefore not fully capturing the current gold rally, which Jarden Research flagged as the main reason revenue came in below consensus.

Capital allocation was active. Northern Star paid a A$347 million dividend, refinanced its undrawn A$1.75 billion bank facility to 2030 and 2031, and announced an on-market buyback of up to A$500 million from 23 April. Net cash sat at A$320 million with cash and bullion of A$1,183 million. Notably, KCGM generated negative net mine cash flow of A$49 million after heavy growth investment, while Jundee remains under operational review aimed at lifting margins, signalling persistent issues there.

Looking forward, the investment case hinges on commissioning the expanded KCGM mill in early FY27, which should structurally lift throughput from 13 to 27 million tonnes per annum and meaningfully lower unit costs across the group. Until then, growth capex remains heavy at A$2,315 to A$2,425 million. Jarden retains an Underweight rating with a A$22.30 target price.