Seagate Technology Holdings plc engages in the provision of data storage technology and infrastructure solutions in Singapore, the United States, the Netherlands, and internationally. The company offers mass capacity storage products, including enterprise nearline hard disk drives (HDDs), enterprise nearline solid state drives (SSDs), enterprise nearline systems, video and image HDDs, and network-attached storage drives.

Seagate Technology (STX) Q3 FY26 Earnings Summary

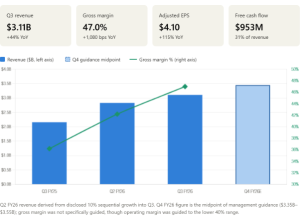

Seagate Technology delivered a standout March quarter, with revenue of $3.11 billion, up 44% year-on-year and 10% sequentially. Non-GAAP earnings per share more than doubled from a year ago to $4.10, while free cash flow reached $953 million, the highest level in over a decade. Gross margins expanded to a record 47% from 42.2% in the prior quarter, and operating margins hit 37.5%. Management issued June quarter guidance well above analyst expectations, calling for revenue of around $3.45 billion and EPS near $5.00 at the midpoint, comfortably ahead of consensus near $3.16 billion and $3.96. The stock jumped roughly 15% in after-hours trading following the release.

The story behind these numbers is almost entirely about cloud and artificial intelligence. Data centre customers accounted for 80% of revenue and 88% of exabytes shipped, with data centre revenue rising 55% year-on-year to $2.5 billion. Seagate has finalised build-to-order contracts that lock in pricing and volumes for nearly all of its high-capacity nearline drives through fiscal 2027, giving unusually strong visibility. Management raised its multi-year revenue growth target from the low-to-mid teens to a minimum of 20%, citing the rapid ramp of its Mozaic HAMR drive platform, which is now qualified at 75% of leading global cloud customers.

Profit growth is being driven by a richer mix of high-capacity drives and disciplined pricing rather than higher unit volumes. Management was clear that total drive units are not growing, and would actually be declining if not for some older PMR shipments helping fill the gap. Average revenue per terabyte rose in the mid single digits year-on-year, and incremental gross margins are running above 70%. Fitch upgraded the credit rating to investment grade after Seagate retired $641 million of debt during the quarter, taking gross debt to $3.9 billion and net leverage to just 0.7 times.

For investors, the risks deserve equal attention. Customer concentration is high, with hyperscale cloud providers dictating most demand, while edge and consumer revenue grew only 2% sequentially. With capacity already allocated through 2027, Seagate cannot easily flex up further if demand surprises. The shares have more than doubled this year, so much of the good news is priced in, and any slowdown in cloud capital spending or execution stumbles on the next-generation Mozaic 5 ramp could see the stock derate sharply. The current results are exceptional, but valuation now demands continued flawless execution to justify the share price.