Alphabet Inc., the parent of Google, has delivered a robust second-quarter result that exceeded expectations across revenue and earnings, but investors are now turning their attention to the company’s ambitious capital spending plans.

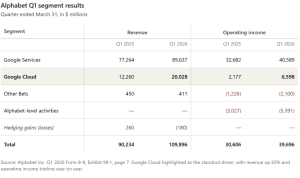

Alphabet delivered a standout first quarter for 2026, with consolidated revenue rising 22% to $109.9 billion and operating income climbing 30% to $39.7 billion. The operating margin expanded to 36.1%, marking the company’s eleventh consecutive quarter of double digit revenue growth. Shares jumped roughly 7% in after hours trading, the strongest reaction among the four big tech names that reported on the same day.

The headline story is Google Cloud, where revenue accelerated sharply to $20.0 billion, up 63% from a year earlier. Cloud operating income tripled to $6.6 billion, and the order backlog nearly doubled in just three months to $462 billion, suggesting customers are locking in long term commitments for AI infrastructure and tools built on Alphabet’s Gemini models and custom chips. Google Search revenue also grew a healthy 19% to $60.4 billion as artificial intelligence features drove higher usage and record query volumes.

Investors should view the headline net income figure of $62.6 billion, up 81%, with some caution. Around $36.9 billion of pre tax other income came from unrealised paper gains on equity investments, widely reported to relate primarily to Alphabet’s SpaceX stake. After tax, this contributed roughly $28.7 billion to reported net income, meaning the underlying operating earnings growth, while strong, is far less dramatic than the reported earnings per share figure of $5.11 implies.

Capital expenditure more than doubled to $35.7 billion in the quarter, and management raised full year guidance to between $180 billion and $190 billion, with a further significant increase signalled for 2027. Free cash flow fell to $10.1 billion as a result. YouTube advertising growth of 11% slightly missed expectations, Google Network revenue declined nearly 4%, and Other Bets losses widened to $2.1 billion despite Waymo surpassing 500,000 weekly autonomous rides. Long term debt nearly doubled to $77.5 billion following a fresh bond issuance, while share buybacks paused entirely during the quarter.

The investment case ultimately rests on whether the enormous AI infrastructure spending generates returns matching the growing cloud backlog. So far the numbers support the strategy, but execution risk rises with each capex increase. A 5% dividend lift to $0.22 per share offers modest income support for shareholders.