The Reserve Bank of Australia raised the official cash rate by 25 basis points to 4.35 per cent on Tuesday, marking the third consecutive hike this year and fully reversing the modest easing cycle that ended in late 2025.

The decision passed in an 8 to 1 board vote, with one member preferring to hold at 4.10 per cent. Markets had priced roughly a 74 per cent probability of a hike heading into the meeting.

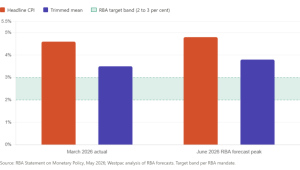

Two forces drove the decision. First, domestic capacity pressures had already pushed inflation higher through the back half of 2025, with headline CPI reaching 4.6 per cent in the year to March and the trimmed mean measure of underlying inflation sitting at 3.5 per cent. Both readings remain well above the 2 to 3 per cent target band. Second, the conflict in the Middle East has resulted in sharply higher fuel and related commodity prices, which are already adding to inflation, with shipping disruptions in the Strait of Hormuz feeding directly into Australian fuel costs. The RBA flagged early signs that many firms experiencing cost pressures are looking to increase prices of their goods and services, a classic second round effect that risks entrenching inflation expectations.

The accompanying Statement on Monetary Policy delivered sobering forecasts. Headline inflation is expected to peak at 4.8 per cent in the June quarter 2026, while underlying trimmed mean inflation is expected to remain above 3 per cent until mid 2027. Inflation is not seen returning to the 2.5 per cent midpoint of the target band until mid 2028, roughly two years later than previously hoped. The forecasts also embed an assumed cash rate path that climbs to 4.7 per cent by the end of 2026, suggesting at least one further hike is likely.

The economic costs are starting to show. The unemployment rate is forecast to increase to 4.7 per cent by mid 2028, up from 4.3 per cent today, and GDP growth has been revised lower as fuel prices erode real household incomes. Major lenders including NAB and Commonwealth Bank moved swiftly to pass the increase through to variable mortgage rates within weeks.

Investors should weigh several uncomfortable realities. The RBA baseline rests on the Middle East conflict resolving relatively soon and oil prices receding. Westpac economists see trimmed mean inflation peaking at 4 per cent and staying there for the remainder of 2026. Deputy Governor Andrew Hauser has openly warned of a stagflation scenario where inflation accelerates even as growth weakens. Productivity assumptions also look optimistic, requiring a sharp turnaround from 0.9 per cent annual growth in 2025 to flat readings into mid 2026.

Rate sensitive sectors such as housing, discretionary retail and small caps face an extended period of pressure. Variable rate borrowers should budget for the possibility that 4.35 per cent is not the peak. Defensive positioning and quality balance sheets are likely to outperform until the inflation trajectory becomes clearer.