US equities closed lower on Tuesday, although pared back larger initial losses as investors await two days of semi-annual testimony by Federal Reserve Chairman Jerome Powell before Congress.

United States

The S&P 500 fell along with the Dow -0.71%, the Nasdaq Composite slipped by -0.16 while the Russell 2000 Index receded -0.47% and the VIX was -2.18% lower at 13.88. The yield on the 2-Year treasury bond was -2.7 basis points lower at 4.688%, and the yield on the 10-Year bond also weakened 4 basis points to 3.724%. Shares in FedEx slumped as much as -5% in after-hours trading after providing a 2024 outlook that fell short of analyst estimates on weakening demand.

The market rally last week was largely driven by an AI frenzy, which experts on Wall Street are taking a precautionary stance. A global markets strategist at Citigroup, Scott Chronert commented, “The issue is going to be: to what degree does that show up in fundamentals?” Regarding Powell’s upcoming speech, Lisa Shalett, the chief investment officer at Morgan Stanley Wealth Management noted, “If a favourable soft landing does materialize, the Fed will have no incentive to cut rates, especially if labour markets are still relatively resilient.”

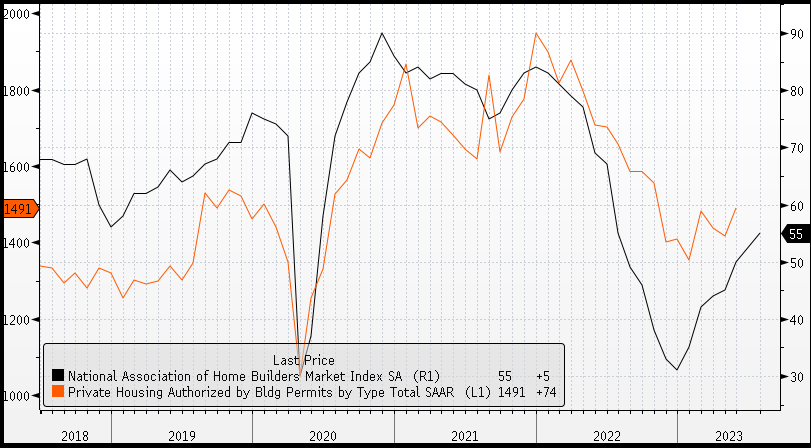

In economic data, the Wells Fargo Housing Market Index (NAHB) rose to 55 in June, a sizeable beat compared to estimates of a more modest increase to 51 from 50 previously. Coupled with a strong increase in building permits of 5.2% over the month, also significantly exceeding estimates, the data points to a potential turning point in the housing market which has been weighed by the Federal Reserve’s policy tightening.

NAHB Housing Index/Building Permits

Europe

European equities were also lower, likely weighed by stimulus from China which has fallen short of expectations. The Euro Stoxx 600 Index closed -0.59% lower on Tuesday with eight out of the eleven sectors closed in the red. Energy was the biggest underperformer, falling -1.38%, the materials sector fell by -1.22% and consumer discretionary was down -1.22%. The CAC slid -0.27%, the DAX retreated -0.55%, while the FTSE was down by -0.25%.

The focus tonight in economic data centres around the United Kingdom, with inflation data for May due to be released at 16:00 AEDT. Consensus estimates are for core prices to remain unchanged at 6.8% while headline prices are expected to show a slight moderation to 8.4% from 8.7% previously.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

Australia

The ASX is set to open lower, with ASX Futures down -29 points or -0.39% to 7,307. The Index closed 0.86% higher at 7,357 following the release of the RBA policy minutes which were less hawkish than expected. The minutes showed the board has considered holding the cash rate at 3.85%, and unlike previous minutes there was no talk of whether further rate hikes were needed. This suggests the board is becoming increasingly uncertain on the outlook for policy and is interpreted as dovish leaning. The policy sensitive 3-year bond yield declined -2.8 basis points with the Australian Dollar falling -0.996% to 0.6785 following the minutes, although there was little change in interest rate expectations with futures markets still pricing in nearly a further 0.5% of tightening by year end. In focus today is the release of the Westpac leading index for May due at 11:00 AEDT.

The benchmark index saw broad-based buying with 73.5% of stocks finishing higher on Tuesday. Energy rallied by 1.94%, real estate jumped 1.34% while financials gained 1.19%. Healthcare was the only underperforming sector, finishing little changed. In energy, shares in Santos rose 2.25% along with Woodside 2.22%, Paladin 1.37%, and Whitehaven 0.59%. In financials, Magellan financials rocketed 5.84%, Westpac firmed 1.32%, CBA gained 1.10%, while Block bucked the trend by sliding -0.14%. Lake Resources was the biggest underperforming stock, plummeting -19.74% after falling -20% on Monday.

Commodities

In commodities, oil prices declined after China’s stimulus measures fell short of expectations. The price of WTI and Brent crude fell by -1.03% and -0.84% to $71.19 and $75.45 respectively. The prices of precious metals receded on Tuesday, with spot gold falling by -0.72% to $1936.42 while the price of spot silver sank by -3.42% to $23.14. Industrial metals were weaker, the price of copper was down by -0.14% at $388, nickel sank by -2.41% to $22,402, and SGX Iron Ore rose declined by -0.774% and are a further -1.6% lower this morning at US$111.20. Meanwhile, bitcoin rallied 5.4% to $28,143 with the increase attributed to news of BlackRock filing for a spot Bitcoin ETF with the SEC.

Economic Calendar

21st June 2023

BoJ Monetary Policy Meeting Minutes 09:50

Australian Westpac Leading Index (MoM May) 11:00

US Fed Chair Powell Testimony 00:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via [email protected] or by phoning +612 8302 3632.