ANZ Group Holdings Limited engages in the provision of banking and financial products and services to retail and business customers in Australia and internationally. The company operates through three segments: Personal, Business & Agri, and Institutional. It offers banking and wealth management services to consumer and private banking customers; banking services to small and medium enterprises, and the agricultural business.

ANZ delivered a headline cash profit of $3.78 billion for the half year to March 2026, up 6% on the prior corresponding half and a substantial 70% rebound on a September 2025 period that was weighed down by restructuring charges and regulatory settlements. The interim dividend was held at 83 cents per share, partially franked at 75%, and return on tangible equity recovered to 11.6%.

The improvement was driven primarily by lower operating expenses, which fell 4% on the prior comparative half as the bank pushed through productivity initiatives and reduced headcount by around 2,500 full time staff. Credit impairment charges of $274 million were also lower than many analysts expected. These are real wins, but they are not a substitute for revenue growth, and that is where the result starts to look thinner.

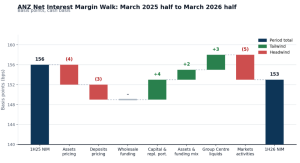

Net interest income was essentially flat year on year at $8.89 billion. The net interest margin, which measures how much the bank earns on its lending after funding costs, contracted by 3 basis points to 1.53%. Competition for both loans and deposits continue to bite, and the gross loan book actually shrank slightly to $825.7 billion. Other operating income did rise 9%, but a meaningful portion came from Markets trading and foreign currency hedging gains, which tend to be lumpy rather than recurring.

Source: ANZ Group Holdings 1H26 Consolidated Financial Report, page 18.

The divisional picture was uneven. Institutional banking remained the largest profit contributor at $1.35 billion, though it slipped 2% on the prior year. Australia Retail produced a strong $945 million result helped by a sharp drop in restructuring costs. Suncorp Bank profit fell 10%, while New Zealand and the Business and Private Bank divisions were broadly steady.

Capital and credit settings remain comfortable. The CET1 ratio sits at 12.4%, providing flexibility to fund future growth, although collective provisions as a share of credit risk weighted assets are still below where some peers sit, which is a watchpoint as economic conditions evolve.

Looking ahead, the cost and credit benefits delivered this half are largely banked. The harder question for shareholders is whether ANZ can lift the revenue line through stronger lending growth and stable margins.