The latest monthly estimate of inflation for November has been released this morning, coming in well below market forecasts.

The latest inflation estimate for November was released this morning, with headline prices coming in modestly below expectations.

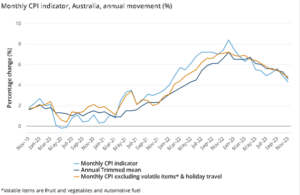

For the 12-months to November, headline prices rose 4.3% vs 4.4% estimated by economists, down from 4.9% previously. When excluding volatile items, prices rose 4.8% down from 5.1% in October. While prices remain above the RBA’s 2-3% target, the chart below highlights that the trend is clear, inflation pressures continue to ease.

Source: Australian Bureau of Statistics

The latest inflation print adds to the case that the headwind of rising interest rates will continue to be removed from risk assets in 2024, pending no resurgence inflation. While markets are only pricing in two rate cuts for 2024, it is not only the speed by the direction which matters for investors. As financial condition ease, the labour market continues to remain relatively resilient, and should the economy pick up as expected in the latter half of 2024, the backdrop remains favourable for higher equities and lower bond yields.

Given the reading was mostly in line with expectations, financial markets are little changed. The Australian Dollar is 0.04% higher at 0.6690, the ASX200 is -0.2% lower but off its session lows, and 2-year government bond yields are -2 basis points lower at 3.824%.

The latest data follows the RBA’s surprise rate hike in November to bring the cash rate to 4.35%, which many now view as a mistake given weaker-than-expected GDP data since then and the continued decline in inflation. The RBA will certainly be waiting for the official Q4 inflation data due on January 31st before making an decisions on policy at its next meeting on February 6th.

Financial markets continue to price that the RBA is done with its tightening campaign and will need to ease rates in 2024 to cushion a slowdown in economic growth with GDP expected to slow to 0.2% in Q4 23 and grow at 0.3% in each of the first two quarters of 2024 before picking up again.

The latest inflation print adds to the case that the headwind of rising interest rates will continue to be removed from risk assets in 2024, pending no resurgence inflation. While markets are only pricing in two rate cuts for 2024, it is not only the speed by the direction which matters for investors. As financial condition ease, the labour market continues to remain relatively resilient, and should the economy pick up as expected in the latter half of 2024, the backdrop remains favourable for higher equities and lower bond yields.

We should not that we believe interest rates are unlikely to return to the ultralow levels in the wake of the COVID-19 pandemic, but rather settle around more historically normal levels around 3% with markets implying a policy rate of around 3.3% in 2-years from now.