Johnson & Johnson (JNJ) is a current holding within the US Starter Pack.

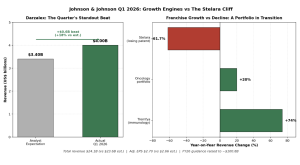

J&J delivered a clean beat across the board. First-quarter revenue of $24.1 billion rose nearly 10% year on year and comfortably exceeded the $23.6 billion consensus, a beat of roughly $500 million. Adjusted earnings per share of $2.70 edged past the $2.66 analyst forecast. The company also raised its full-year 2026 revenue guidance to a midpoint of approximately $100.8 billion, slightly above the $100.6 billion the street had been modelling, and lifted adjusted EPS guidance to a $11.55 midpoint.

The single biggest surprise in the report was Darzalex. The blood cancer treatment generated approximately $4 billion in quarterly sales, massively ahead of the $3.4 billion analysts had penciled in. That is an 18% beat on one of J&J’s largest individual drugs, and the dominant reason the overall revenue line exceeded expectations. The broader oncology portfolio, which includes Carvykti, Tecvayli, and Talvey, contributed around $5 billion in total and grew roughly 20% year on year.

Tremfya was the other standout, with sales climbing 74% year on year as the drug expanded its use into inflammatory bowel disease indications. This franchise is increasingly central to the pharmaceutical business and outpaced analyst expectations.

The offset was Stelara, where revenue collapsed 61.7% to just $656 million as biosimilar competition accelerated. This was largely anticipated by analysts, but the severity of the decline is still striking in absolute terms. Importantly, J&J’s growth engines more than covered the Stelara hole, which is why the overall revenue beat was achievable at all.

The MedTech segment, covering surgical equipment and orthopaedics, delivered another steady contribution in line with or slightly ahead of expectations, reinforcing the diversification advantage J&J holds over pure pharmaceutical peers.

The mild caution inside the headline beat: adjusted EPS still fell 2.5% year on year despite beating consensus, the guidance raise was modest rather than aggressive, and the company faces real risk from US drug pricing policy and tariff-related supply chain costs. The dividend was raised 3.1% to $1.34 per share, marking 64 consecutive years of increases, which is a meaningful vote of confidence from management. Overall, this is a higher quality beat than GS in some respects because the guidance raise implies that management expects the momentum to continue, rather than the quarter being a volatility-driven spike.