Lam Research Corporation designs, manufactures, markets, refurbishes, and services semiconductor processing equipment used in the fabrication of integrated circuits in the United States and internationally.

Lam Research delivered a strong March quarter, with revenue of $5.84 billion climbing 24 percent year on year and comfortably clearing Wall Street’s $5.75 billion estimate. Adjusted earnings per share reached $1.47, well above the $1.37 consensus and up from $1.27 in the prior quarter. The headline numbers landed at the upper end of company guidance, and investor reaction was positive but restrained, with shares rising around 2.5 percent after hours as expectations heading into the print were already elevated after a strong run.

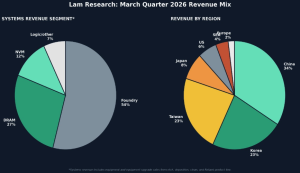

The standout story was the Customer Support Business Group, which crossed two billion dollars in quarterly revenue for the first time, reaching $2.11 billion and growing 25 percent from a year earlier. This services and upgrades business tends to be more stable than core equipment sales, so hitting that milestone points to a larger installed base at chip customers and more recurring revenue. Systems revenue, the core equipment piece, came in at $3.73 billion, up 23 percent year on year but slightly below the $3.75 billion estimate, the only notable blemish in an otherwise clean beat. Foundry customers drove 54 percent of systems sales, with memory close behind at 39 percent.

Lam attributes the momentum to artificial intelligence demand, which is pushing chipmakers to invest heavily in new NAND, DRAM, and foundry capacity. Management raised its industry spending forecast for 2026 to around $140 billion with a bias toward further upside, and expects second half revenue to exceed the first half. June quarter guidance reinforced this, with revenue projected at $6.60 billion give or take $400 million and EPS at $1.65 give or take 15 cents, both meaningfully above consensus. Gross margin is guided to expand toward 50.5 percent. Lam also returned more than $1.1 billion to shareholders through buybacks and dividends.

Underneath the optimism, investors should note cautionary signals. Capital expenditure jumped to $332 million, roughly fifty percent higher than expected, which dented free cash flow to $810 million despite healthy operating cash generation. The spike signals aggressive capacity investment, a positive for growth but a potential margin risk if demand softens. China accounted for 34 percent of revenue, the largest single region, keeping geopolitical and export control risk firmly in play. Deferred revenue also edged lower this quarter.