Since our last market update at the end of October, there have been several key developments in financial markets, which are covered daily in the Morning Market Wrap. With the end of year approaching this is a good time to update on what has transpired and the outlook for equities leading into 2024.

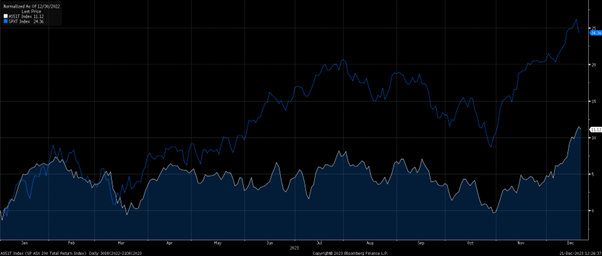

Major equity markets bottomed at the end of October, initially rallying having become heavily oversold, with fuel added to the rally following economic data and the central bank signalling that they would likely switch to an easing stance in 2024. This has significantly benefited several of Rivkin’s portfolios, notably ASX Blue Chips has climbed 13.82%, ASX Growth has jumped 14.19%, and US Growth has gained 14.12%.

S&P500 & ASX200 YTD %

Most notable was the Federal Reserve’s pivot at the December 14th meeting, where officials projected more rate cuts for 2024 than in their September projections. Chair Jerome Powell’s language also softened significantly, signalling to the market that cutting rates was likely in 2024.

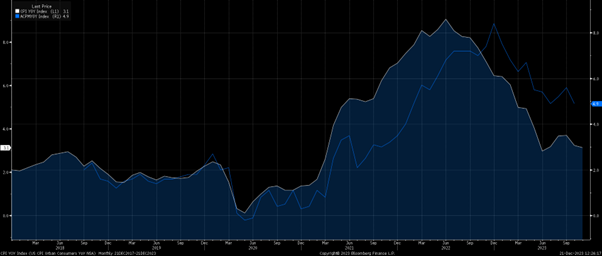

This is due to the changing balance of risks for the Fed, and other central banks. With inflation now sustainably trending down towards targets, the risk for central bankers increasingly shifts towards avoiding too much economic pain and keeping rates too restrictive for too long. US inflation peaked at 9.1% back in June 2022 and now sits at 3.1% on a year-on-year basis. There is a similar story here in Australia, with inflation now at 4.9% having peaked at 8.4% in December 2022. Unemployment is also beginning to trend higher, although not overly concerning at this point. Central bankers know that policy works with a lag and it is likely that unemployment will continue to edge up and inflation move down towards target. There are of course risks to this view, and inflation can always rebound or prove stickier and take longer to bring down. What is important for investors is expectations and the trend lower, which are in the supportive side of the ledger for equities.

Aus & US Inflation

The US economy also continues to prove surprisingly resilient, with the latest Atlanta Fed GDP Nowcast pointing to a 2.68% annualised rate of growth for the current quarter. This is well above the consensus estimate of economists at 1.1%, and expectations are clear for a slowdown at the start of 2024 before picking up in the latter half of the year. A change to easier monetary policy is a significant boost to hopes of a “goldilocks” scenario occurring, where economic growth continues at a decent pace, inflation cools, and the labour market isn’t severely damaged. Such an outcome would be highly supportive for equities, and a similar analogy would be the Fed pivot at the end of 2018 which saw the S&P500 gain nearly 40% within 12 months.

The story here in Australia is similar, although having raised interest rates by less than other central banks, RBA officials continue to push back against market pricing. Again, the trend here is clear, inflation is moving lower and the latest GDP reading for Q3 at 0.2% was well below expectations. This is meaningful and investors expect the RBA will need to also shift to an easing stance in 2024, currently pricing in 2.5 rate cuts for 2024 which would bring interest rates back down to 3.72%. Growth in Australia is also expected to cool over the coming quarters, troughing at 0.2% in Q4 before picking up to 0.5% by Q3 2024.

On to the outlook for 2024, with central banks switching to an easing stance and economic data expected to pick up in the latter half of 2024, the outlook is optimistic. Investors are forward-looking by around 6-12 months, and forecasts are certainly positive in terms of earnings and economic data. We have also seen significant signs of internal strength within the market, several key measures of breadth point to the solid potential for sustained gains, typically over the following 6-12 months. In the short term, given how stretched equities have become it would be unsurprising to see short-term weakness, which is a healthy development. After all, equities don’t move in a straight line.

In our view, it is increasingly likely we will see a soft landing, particularly in the United States, with a goldilocks scenario emerging. This can always change, and we need to monitor incoming developments. Given the significance of the Federal Reserve’s pivot, the environment is like to remain one of buying the dips.