Microsoft (MSFT) announced Q2 earnings results overnight, and while the stock is not a current holding in any of the Rivkin portfolios, it is a company which attracts the attention of investors globally.

While Q2 results were positive and headline numbers topped analyst estimates, shares declined as much as -2.84% in after-hours trading, with sentiment seemingly weighed by slower growth in the Azure cloud services business and capital expenditure which exceeded estimates. Revenue exceeded analyst estimates, posting an actual of USUS$56.19 bn vs USUS$55.49 bn. The company’s broad software portfolio has been instrumental in these favourable results, taking advantage of the digital transition as companies modernize their IT infrastructures.

A breakdown of the earnings report shows consistent growth in all major segments. The productivity and business processes division reported revenue of US$18.29 billion, surpassing the predicted US$18.1 billion, while the intelligent cloud division recorded US$23.99 billion, beating the estimated US$23.8 billion. Similarly, more personal computing posted a revenue of US$13.91 billion, ahead of the US$13.58 billion projection. This positive trend is also reflected in the reported earnings per share of US$2.69, up from US$2.44 and a beat of 5.28% compared to forecasts of US$2.555.

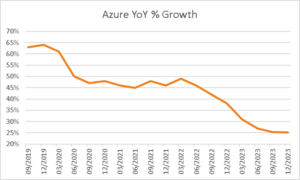

While these numbers point to a strong financial position, Microsoft’s path to growth isn’t without challenges. Despite promising interest in new AI-driven products, the company saw a lukewarm response in terms of sales growth for its Azure cloud-services business which slowed from 31% the prior quarter to 27% year-on-year. Despite the cloud service’s growth slowing down, it still represents a significant portion of the company’s total revenue, contributing to more than half to Microsoft’s total US$110 billion of cloud-related revenue for the first time in 2023.

Nevertheless, the company sees potential in its AI capabilities, with CEO Satya Nadella announcing several new AI programs powered by models from OpenAI, aiming to address the strong market demand for internet-based services. While the revenue increase from these programs may not be immediate, a gradual rise is expected and includes new products, such as Microsoft 365 Copilot, a new suite of AI tools priced at US$30 per month per user.

However, the focus on growth and innovation comes with increased expenses, with capital expenditure reaching US$8.94 billion, above the estimated US$7.85 billion. These costs are attributed to the expansion of data centres and the acquisition of chips required for complex AI systems.

While the market reacted negatively to the report, there’s still an optimistic outlook for Microsoft shares. The company’s strategic investments, growing customer base, and strong foothold in the rapidly advancing AI industry position it well for future growth. The comprehensive transformation of Microsoft’s products around OpenAI’s GPT-4 language model and the ongoing demand for digital transformation across industries highlight the potential for more substantial revenue gains in the coming years. Despite short-term market reactions, Microsoft’s long-term prospects remain promising which is supported by 87% of analysts maintaining a buy recommendation on the stock, with a 12-month price target of US$377.80 implying 7.6% upside from current levels.