NVIDIA Corporation, a computing infrastructure company, provides graphics and compute and networking solutions in the United States, and internationally.

Nvidia delivered another blockbuster quarter, but beneath the headline numbers lie important nuances that retail investors should understand before getting swept up in the momentum with shares initial rising as much as 4% before trading 1.25% higher in after-hours.

The chipmaker reported fiscal fourth quarter revenue of $68.1 billion, a 73% increase from the same period a year ago, comfortably beating Wall Street’s expectation of $65.9 billion. Earnings came in at $1.62 per share on an adjusted basis, also topping the $1.53 consensus estimate. Perhaps more importantly, Nvidia guided first quarter revenue to approximately $78 billion, well above the $72.8 billion analysts had expected, sending shares up roughly 4% in after hours trading. While these numbers are undeniably impressive, it is worth noting that the rate of growth is naturally decelerating from the triple digit surges seen in earlier quarters, a mathematical inevitability as the revenue base expands.

The data center division remains the overwhelming engine of growth, generating $62.3 billion in revenue, or roughly 91% of the total. Within that segment, networking revenue was particularly notable, surging to $11 billion from just $3 billion a year ago, reflecting the growing complexity of AI infrastructure buildouts. This networking strength is strategically significant because it deepens customer dependency on Nvidia’s full ecosystem rather than just individual chips, creating switching costs that competitors will struggle to overcome. Adjusted gross margin held strong at 75.2%, meaning Nvidia keeps about 75 cents of every dollar after production costs, a remarkable level that speaks to its pricing power and near monopolistic positioning in AI accelerators.

However, not everything was rosy. Gaming revenue of $3.73 billion missed estimates of $4.01 billion, and automotive sales of $604 million also fell short of the $643 million expected. These segments, once core to Nvidia’s identity, are increasingly overshadowed by AI. This raises a subtle but important question: is Nvidia becoming a one product company? When over 90% of revenue comes from a single division, the business becomes highly sensitive to any slowdown in AI capital expenditure cycles. Adjusted operating expenses jumped 51% year over year to $5.1 billion, and the forward guidance projects these rising to $7.5 billion, significantly above analyst expectations of $5.33 billion. That spending trajectory deserves serious attention, as it suggests Nvidia is investing aggressively to maintain its lead, which could pressure margins over time and signals that management sees the competitive landscape intensifying.

Two significant external risks loom. First, Nvidia excluded any China data center revenue from its first quarter outlook amid ongoing US export restrictions, meaning one of the world’s largest markets remains effectively off limits for its best products. The recent H200 licensing arrangement comes with cumbersome inspection requirements and a 25% tariff, making it commercially unattractive at scale. Second, a global shortage of memory chips threatens to constrain how many systems Nvidia can actually ship, though the company claims it has secured enough supply for the near term. Investors should treat that assurance cautiously, as supply chain visibility tends to shorten quickly when industry wide shortages escalate.

The broader concern for investors is concentration risk on the demand side. Mega deals with companies like Meta for millions of processors sound impressive, but critics have flagged that some of these arrangements involve circular financial relationships between suppliers and customers, potentially inflating demand signals. If a handful of hyperscalers ever pause or slow their AI spending simultaneously, the revenue impact on Nvidia would be severe and sudden. Free cash flow of $34.9 billion, more than double the prior year, provides a substantial cushion, but investors should remember that Nvidia’s current valuation already prices in years of continued exceptional execution.

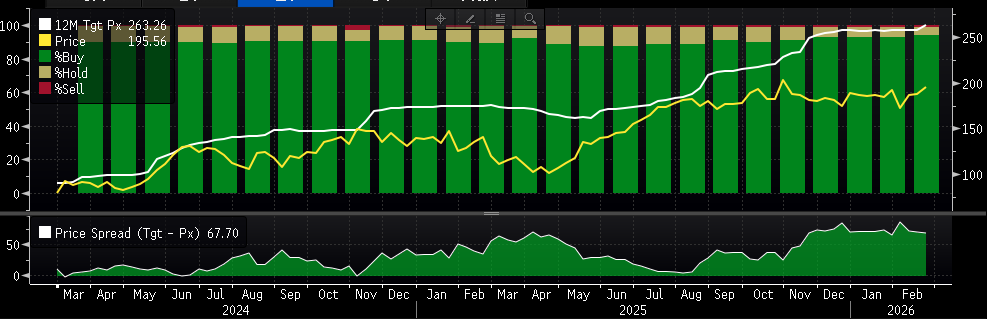

This visual is the most telling for retail investors. With 94% of analysts rating Nvidia a “buy” and a consensus 12 month price target of $263.26 versus the current price of $195.56, it illustrates both the overwhelming bullish sentiment and the implied 34.6% upside. However, near unanimity among analysts can itself be a contrarian warning signal. When virtually everyone agrees, the risk of disappointment becomes asymmetric, meaning the downside surprise potential may be greater than the upside. It is also notable that Nvidia has been among the 10 worst performing chipmaker stocks so far this year despite consistently beating estimates, suggesting the market is beginning to demand more than just earnings beats to justify the valuation. The gap between analyst optimism and recent price action tells a story of a market that is growing more discerning about how much future growth is already baked into the share price.