Rio Tinto Group is a British-Australian multinational company that is the world's second largest metals and mining corporation (behind BHP).

Rio Tinto’s Q1 2026 production update shows the mining giant making operational progress, though the quarter was marked by some setbacks. Copper equivalent output rose 9% year-on-year, driven largely by the continuing ramp-up of the Oyu Tolgoi underground copper mine in Mongolia and steady aluminium performance.

The most sobering detail was around safety. Two workers died during the quarter, one at the Simandou iron ore project in Guinea and another at Kennecott in Utah. Both sites were temporarily shut and have since restarted. This is a serious reminder that Rio’s safety record remains imperfect and should not be treated as a footnote, particularly for investors weighing operational risk.

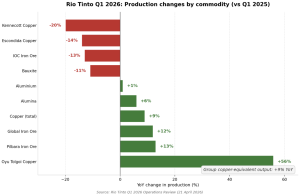

On the numbers, Pilbara iron ore was the operational standout, with production up 13% year-on-year to 78.8 million tonnes, the second-highest first quarter since 2018. However, sales rose only 2% because two tropical cyclones disrupted shipments by roughly 8 million tonnes. The company expects to recover about half of that over the rest of the year, meaning some revenue should still land in 2026 but some is gone for good. The first full shipment of high-grade Simandou ore also reached China, with initial sales realised in April.

Copper production climbed 9%, but the picture underneath is mixed. Oyu Tolgoi surged 56% as its underground mine matures, yet Kennecott was down 20% on unplanned smelter maintenance and Escondida fell 14% on planned lower ore grades. Aluminium volumes held up despite weather-hit bauxite operations, and lithium output reflected the recent Arcadium acquisition, with two new projects, Fenix 1B and Sal de Vida, achieving mechanical completion as planned. Rio also finalised the long-awaited Resolution Copper land exchange in Arizona, unlocking drilling on one of the world’s largest untapped copper deposits.

The pricing backdrop was a genuine tailwind. Average quarterly copper prices jumped 16% quarter-on-quarter, aluminium 13%, and lithium carbonate a striking 84%, partly because the ongoing Middle East conflict is tightening global supply. Iron ore was flat around $104 per tonne. Tariff costs on US-bound aluminium eased slightly on lower shipment volumes.

The cost-out program delivering $650 million of annualised savings is fully implemented. Full-year 2026 production and cost guidance across every commodity was left unchanged, reassuring but offering no upgrades despite the strong quarter.

Overall, operationally solid with welcome price tailwinds, but iron ore shipment shortfalls, Kennecott’s weakness, and the two fatalities temper an otherwise encouraging start to the year.