The global uranium market is now experiencing a robust revival.

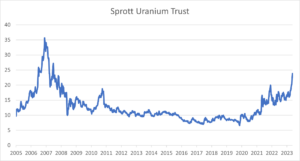

Notably, after a period of stability, prices surged significantly in 2022 and observed a further 20% growth in 2023. Market analysts predict this upward momentum to persist, driven by imminent supply shortages and escalating demand. This market transformation is underpinned by several developments:

- Prioritizing Energy Security: Geopolitical instabilities, exemplified by events such as Russia’s incursion into Ukraine, have heightened concerns over potential supply interruptions. Nations are actively seeking dependable and long-term energy solutions to safeguard against unforeseen supply-chain disruptions.

- Embracing Nuclear Energy: As the world intensifies its efforts to combat climate change, nuclear energy, a zero-emission source, is garnering renewed interest. With countries racing to reduce their carbon footprint, nuclear power offers a viable solution to meet energy demands without exacerbating environmental concerns.

- Mining and Production Challenges: Years of depressed uranium prices have led to reduced investments in mining operations. Now, as demand spikes, these industries are struggling to hit their production targets, leading to potential supply deficits in addition to closed-end trusts removing supply from the spot market.

Below we present a trade idea rather than an official recommendation given this does not meet the criteria for Rivkin’s current portfolios:

There are several ways for investors to gain exposure to this theme, such as individual names listed on the ASX including Paladin Energy (PDN) and Boss Energy (BOE). However, the easiest way is through a diversified ETF, recently listed in Australia, the BetaShares Global Uranium ETF (URNM). For those investors that have access to international markets, the Sprott Physical Uranium Trust (U-U) in Canada, or Yellow Cake PLC (YCA) listed in the UK provide exposure to physical prices, which offer different risks and rewards. In our view, a good way to play this theme would be to split exposure between URNM and U-U/YCA. Given the highly volatile nature of these stocks, a small allocation of ones portfolio to this theme is prudent.

While the prices of these investments have recently shot up, we believe that prices have significant potential in the coming years given. A halt in prices now would be akin to driving 100 km/h on a highway, taking your foot off the accelerator, and expecting the car to immediately stop. There will undoubtedly be corrections and pullbacks along the way, likely providing better entry opportunities for investors to scale in exposure. It is worth noting that the all-time peak in uranium prices, prior to the disaster in Fukushima, was well excess of US$100 per pound, so the recent rally in prices still leaves plenty of upside should the new market dynamics drive uranium towards all-time highs. PDN, for example, traded above $8.00 prior to Fukushima, although it’s worth noting that PDN has raised considerable capital since then so it’s not a perfect apples-for-apples comparison.

Global Nuclear Renaissance

The world is warming up to nuclear energy once again. Despite a momentary lapse in reactor constructions in 2022, the subsequent year promises a vigorous rebound. Asia is at the forefront of this nuclear renaissance. China’s aggressive nuclear energy plans, South Korea’s revitalized focus, and Japan’s accelerated reactor projects underscore the continent’s growing nuclear ambitions. Europe and North America aren’t lagging, with countries reaffirming their commitment to nuclear energy through new projects and reactor license renewals.

A considerable portion of this new capacity is anticipated in China. The nation is making aggressive strides towards nuclear energy, seeking alternatives to coal, which presently dominates its energy mix. The current tally stands at 53 operational reactors in China, with 23 under construction, another 23 in the planning phase, and an impressive 168 more proposed. The global count of operational reactors is 436, with 59 more under construction.

Production Dynamics

Meeting the increasing demand necessitates ramping up uranium production—a task easier said than done, particularly with major miners guiding down production and missing production targets in recent years. Immediate supply will be met but by 2024, the market could witness a supply gap of 30-50 million pounds. Trusts like Sprott Physical Uranium Trust and Yellow Cake PLC, which remove physical supply from the market, are inadvertently contributing to this supply/demand imbalance. Notably, demand for uranium is largely inelastic as new reactors are bullt, meaning that demand remains constant despite higher prices. This is because physical uranium prices represent a minimal cost of running reactors.

The World Nuclear Association’s reports shed light on these dynamics, projecting:

- Near doubling of global reactor uranium requirements by 2040.

- Substantial increase in operable nuclear plant capacity, with China leading the charge.

Rise of Small Modular Reactors

The potential of Small Modular Reactors (SMRs), which produce low-carbon electricity and physically are a fraction of the size of a conventional nuclear power plant, has grown in recent years. Compact yet efficient, SMRs offer a versatile solution to the world’s diverse energy needs, especially in regions with restricted grid connectivity. While WNA’s projections place SMR capacity at 31 GW by 2040, while analysts at BMO Capital Markets, recognizing the technology’s expansive applications, estimates a staggering 58 GW by 2030.

The uranium market is showing resilience and potential, promising a more sustainable future. The shift towards green energy, technological advancements in the form of SMRs, and strategic geopolitical decisions will play crucial roles in shaping the industry’s trajectory in the years to come.