A current holding within the ASX Blue Chip portfolio, Westpac (WBC), announced full-year 2023 results yesterday, with investors reacting positively to an increased dividend and buyback announcement offsetting weaker net income.

The bank’s net income rose to $7.20 billion, a 26% increase from the previous year, though just below the estimated $7.33 billion. In a clear move to support shareholder value, WBC raised its final dividend to $0.72 per share and announced a $1.5 billion share buyback after adjusted earnings per share rose to $0.955, surpassing estimates of $0.891.

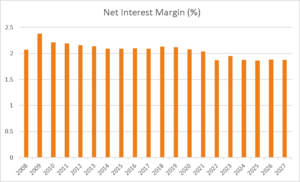

Notably, there was an improvement in net interest margin to 1.95% from 1.93% in 2022 and a core net interest margin increase to 1.87% which had come under pressure across major banks recently following increased competition for the mortgage market. Westpac’s return on equity jumped to 10.1%, and the common equity Tier 1 ratio strengthened to 12.4%, indicating a solid capital buffer above expectations.

However, the second half of the year saw a 20% fall in net income and a slight decrease in net interest margins, hinting at the challenging environment that’s expected to persist into 2024. Despite a decrease in consumer net earnings, growth in business and institutional banking segments paints a picture of a diversified and robust financial institution. Westpac is bracing for economic uncertainties with increased impairment provisions, particularly in the volatile consumer mortgage market.

Westpac’s focus now shifts to maintaining its competitive edge and managing expense growth—a challenge shared across the sector. CEO Peter King’s strategic vision includes a significant transformation project to streamline operations, although he anticipates a multi-year effort amid rising technology costs.

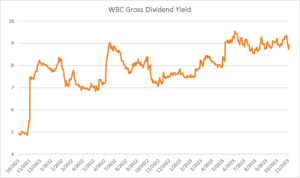

While investors will continue to focus on net interest margins across major banks, with NAB set to report this Thursday, and ANZ next week, they continue to benefit from the higher interest rate environment, as well as what has so far proved a resilient property market. As a reminder, Westpac’s inclusion in the ASX Blue Chip portfolio is based on dividend yield, which currently sits at 8.94% on a gross basis making it one of the higher-yielding stocks within large-cap equities.

WBC remains an active buy/hold recommendation.