With data in the United States, as well as signals from the Federal Reserve, it is increasingly likely that - pending no significant upside surprises in inflation - the central bank has reached a peak in interest rates.

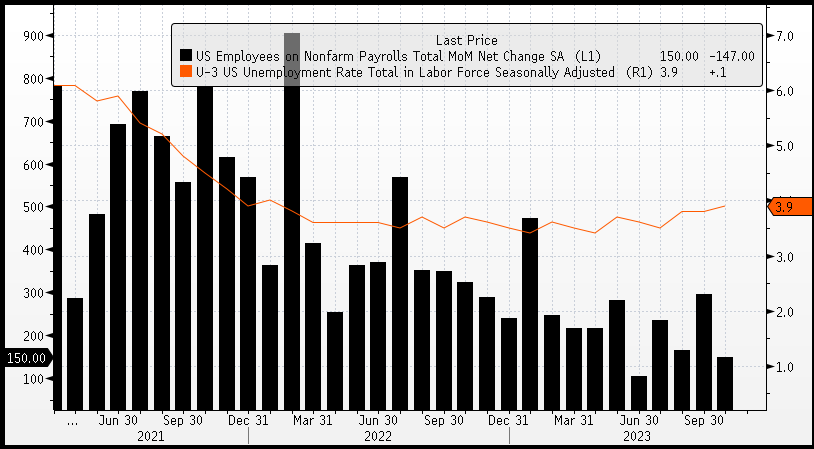

Further data added to this view on Friday, with the latest non-farm payroll report showing 150k jobs were added over the month, below estimates of 180k, while the unemployment rate edged higher to 3.9% from 3.8%. After strong gains post-pandemic, job gains have moderated over the past several months, increasing the likelihood of a “goldilocks” scenario where tighter interest rates cool inflation without causing a severe recession or breaking something in the economy. In fact, initial estimates showed the US economy expanded at a resilient 4.9% over the third quarter, adding weight to the view that a soft landing can be achieved.

There are a few risks to this view: notably, the yield curve is beginning to steepen from deeply negative levels, which historically has preceded recessions although equity market performance has historically been mixed, leading to higher prices in the 80’s and 90’s, with lower prices in the 2000’s. A potential reason that a recession may not follow this time is that the steepening is being driven by longer-term rates as markets price in more resilient growth, while over the past 30 years, steepening has generally been driven by short-term rates as the Federal Reserve reacts as various crises have unfolded.

So, how do equity markets perform after the Federal Reserve finishes its hiking cycle? The table below shows the total returns for the S&P500 over 1, 3, 6, and 12 months after the final rate increase. As we can see, 1-to-3-month periods show mixed results, in line with expectations for equities that markets are more volatile in the short term. Notably, longer-term returns between 6 to 12 months are more promising with higher average returns as well as a positive expectancy with 78% of historical precedents showing a positive 12-month return.

| Date of last hike | 1 Month | 3 Months | 6 Months | 12 Months |

| 5/07/1974 | -4.85% | -24.52% | -13.21% | 18.31% |

| 15/02/1980 | -8.25% | -5.96% | 12.00% | 15.89% |

| 8/07/1981 | 3.11% | -3.37% | -4.25% | -11.25% |

| 18/02/1982 | -2.61% | 3.30% | -1.66% | 37.63% |

| 24/02/1989 | 0.85% | 12.16% | 24.53% | 16.80% |

| 1/02/1995 | 3.55% | 10.04% | 20.53% | 39.19% |

| 16/05/2000 | 0.00% | 1.24% | -5.86% | -11.31% |

| 29/06/2006 | 0.55% | 5.44% | 12.50% | 20.32% |

| 19/12/2018 | 6.68% | 13.57% | 17.93% | 30.45% |

| 23/07/2023 | -2.07% | -6.67% | ? | ? |

| Average | -0.30% | 0.52% | 6.94% | 17.34% |

| % Higher | 60.0% | 60.0% | 55.6% | 77.8% |

We see similar results for the ASX200, although there is a more limited data set, with the ASX200 established in 1992. For this analysis, again we base returns from the Federal Reserve’s last hike, as the US interest rates typically lead those here in Australia. Despite being a limited data set, results are impressive with 12-month periods returning between 14.38% to 32.14%.

| Date of last hike | 1 Month | 3 Months | 6 Months | 12 Months |

| 1/02/1995 | 4.94% | 11.61% | 16.65% | 24.29% |

| 16/05/2000 | 2.34% | 8.89% | 9.52% | 14.38% |

| 29/06/2006 | -0.76% | 4.87% | 16.61% | 32.14% |

| 19/12/2018 | 5.60% | 12.94% | 22.51% | 29.32% |

| 23/07/2023 | -1.80% | -4.62% | ? | ? |

| Average | 2.06% | 6.74% | 16.32% | 25.03% |

| % Higher | 60.00% | 80.00% | 100.00% | 100.00% |

Finally, the following chart shows the 12-month returns for the above table, as we can see with equities there is an upward bias over longer periods, and historically rate pauses by the Federal Reserve have preceded higher equities. Of course, this time can always be different and there are several factors supporting both an optimistic and pessimistic outlook, which is generally the case for equities.