Global equities were lower on Wednesday, weighed by technology shares after Fed Chair Jerome Powell said higher rates were needed to combat inflation, while UK inflation surprised to the upside.

United States

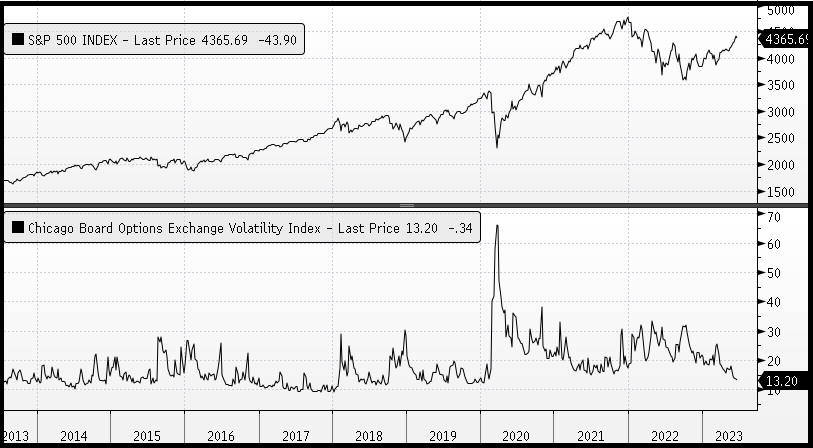

The S&P 500 closed -0.52% lower at the end of trading on Wednesday. The index was weighed down by the information technology sector falling by -1.41%, communications were down -1.35%, and consumer discretionary declined -1.17%. Energy was the star performer, edging up 0.92%, followed by utilities and industrials rising by 0.84% and 0.59% respectively. The Dow Jones closed -0.30% lower, the Nasdaq Composite declined by -1.21% while the Russell 2000 Index was down by -0.20%. Curiously, the VIX which typically has an inverse relationship to equity markets, declined -4.9% to 13.20 reaching levels typically associated with investor complacency that can often coincide with key highs forming. Alternatively, we often see protracted low levels in the VIX during strong bull markets, highlighted by the chart below, and only time will tell which of the current scenarios will prove correct. The yield on the government’s 2-Year treasury bond rose 3 basis points to 4.71%, while the yields on the 10-Year and 30-Year bonds were 3.72% and 3.80% respectively.

S&P500 vs VIX

In the first of two days of semi-annual testimony before Congress, Fed Chair Jerome Powell stated in his speech that a further hike in the cash rate by the Fed for the current year would be “a pretty good guess”. In prepared remarks, Powell noted officials “understand the hardship that high inflation is causing, and we remain strongly committed to bringing inflation back down to our 2% goal” and “Nearly all FOMC participants expect that it will be appropriate to raise interest rates somewhat further by the end of the year”. The weakness in major equity benchmarks were attributed to these comments, however, we must remain mindful that the market has continued to push back against recent hawkish rhetoric, and equites had recently become highly stretched after rallying as much as 16.8% from the March lows, leaving them vulnerable to a correction, which is typically a healthy part of market moves, after all, markets don’t trend in straight lines. Meanwhile, Federal Reserve Bank of Atlanta President Raphael Bostic expressed his views on the hawkish policy, “the bar to justify further rate hikes is higher than it was a few months ago”.

Europe

European shares were also lower, weighed by higher-than-expected UK inflation, as well as declines in US equity markets. The Euro Stoxx 600 closed -0.50% lower on Wednesday, information technology was the biggest laggard, sliding by -1.63%, followed by real estate which lost -1.49% while utilities slipping -0.76%. The energy sector was the star performer, rising 1.34% followed by consumer staples which edged up 0.07%. The CAC closed -0.46% lower, the DAX receded by -0.55% while the FTSE slipped by -0.13%.

The Bank of England will be in the spotlight on Thursday, ahead of an interest rate decision, with economists are forecasting a hike of a quarter of a percentage point to 4.75%. Data on Wednesday showed inflation for the 12 months to May was unchanged at 8.7% while economists had expected a decline to 8.4%. Core inflation surprised to the upside, rising to 7.1% against expectations to remain unchanged at 6.8%. The Bank of England faces a complex outlook, with significant risks of stagflation given the persistence of high inflation and a weakening growth outlook.

UK Inflation (YoY %)

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

Australia

The ASX is expected to open modestly lower this morning with ASX200 futures down -10 points or -0.14% to 7,274. The index declined by -0.58% to close at 7,314 on Wednesday amid broad sector weakness, with only consumer staples 0.71% closing higher. The energy sector was the biggest underperformer losing -1.34%, consumer discretionary was down by -1.2% while materials lost 1.02%. The consumer staple sector bucked the trend, rising by 0.71%. In energy, Woodside and Karoon Energy fell by -1.9% each, while Santos slid by -0.9%. In mining, stocks declined after China’s central bank cut two key benchmark lending rates, Fortescue Metals was down by -1.7%, Rio Tinto lost -1.4% and BHP receded -1.1%. Gold miners experienced a similar decline, Silver Lake Resources sank -5.7%, Northern Star -2.3% and Bellevue Gold fell by -2.8%.

The Westpac leading index for May declined by -0.27% which according to Westpac economists translates to a -1.09% decline in the pace of economic activity over the next three to nine months., which they expect to extend throughout 2023 and into 2024. The yield on the policy-sensitive 3-year bond yield was -3.7 basis points lower at 3.945% while the Australian dollar reversed initial weakness to edge 0.18% higher to 0.6797.

Westpac Leading Index (MoM %)

Commodities

In commodities, the price of WTI and Brent Crude rose by 1.88% and 1.46% to $72.53 and $77.01. The price of precious metals declined, gold fell by -0.20% to 1,932 and spot silver sank by -2.15% to $22.63. In industrial metals, copper added 0.77% to $391 while SGX Iron Ore fell by -2.04% to US$110.70. Extending optimism after the announcement of multiple Bitcoin ETFs, the price of the cryptocurrency climbed a further 6.45% on Wednesday to US$29,985.

Bitcoin

Economic Calendar

22nd June 2023

Fed Waller Speech 18:00

BoE Interest Rate Decision 21:00

US Jobless Claims Report (17th June) 22:30

Fed Bowman Speech 23:55

23rd June 2023

Eurozone Consumer Confidence (MoM Jun) 00:00

Fed Chair Powell Testimony 00:00

USA Fed Barkin Speech 06:30

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via [email protected] or by phoning +612 8302 3632.