Global equities rose on Tuesday following a further easing in US inflation, bolstering bets that the Federal Reserve will soon have reached peak interest rates.

United States

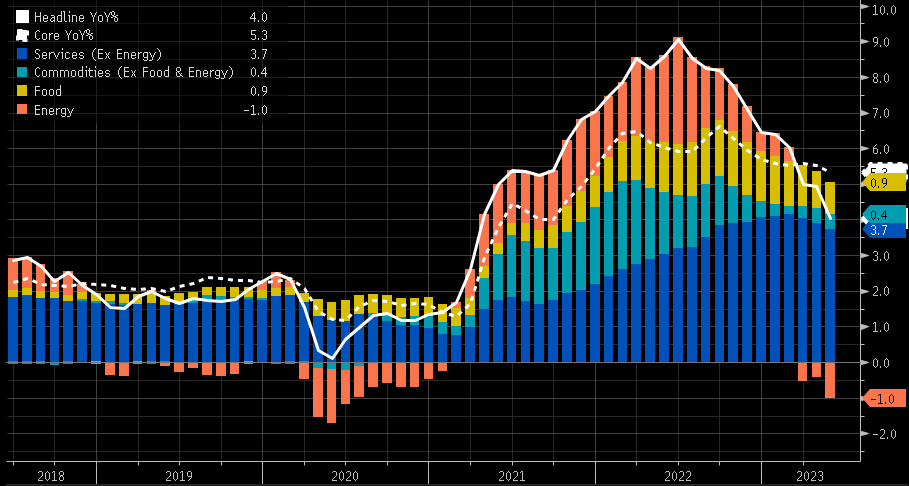

For the month of May, headline inflation rose just 0.1% as forecast amid easing energy prices, while core inflation rose 0.4% as expected, with housing, which is lagging in nature, continuing to keep core prices high. Over the 12 months, core prices easing to 5.3% from 5.5% in line with expectations, with headline prices rising 4% down from 4.9% previously. The so-called “super core” inflation, which measures core prices excluding housing and is closely being monitor by policymakers rose just 0.2% over the month, highlighting the outsized impact on keep core prices sticky, which the effects are expected to gradually roll off. In a further encouraging sign for easing pressures, services inflation which has been a particular concern recently, eased for a third consecutive month after steadily increasing each month since August 2021.

US Inflation (YoY %) source: Bloomberg

The data comes ahead of a policy decision by the Federal Reserve tonight where the central bank is widely expected keep rates unchanged with the probability of a pause based on Fed Fund futures at 88%. Additionally, the central bank will provide updated economic projections or the so-called “dot plots”. Traders continue to price in a likely increase in July of 0.25% sitting at a 60% probability. Given interest rates are in restrictive territory, being higher than year-on-year inflation, one can reasonably argue that a pause in July is a likely scenario, particularly if inflation for June, which is released before the next policy meeting, shows a further easing in price pressures. We know that monetary policy typically operates with a lag of between 6 to 12 months, and if we assume a six-month lag, then a further 1.25% of tightening since November 2022 is yet to show up in economic data, only adding to the case for the central bank to pause and assess how data develops.

Fed Funds vs Inflation (YoY %) source: Bloomberg

The S&P 500 closed 0.69% higher on Tuesday amid broad-based buying with 79% of stocks trading higher. Materials was the star performer, jumping 2.33% after actions the People’s Bank of China unexpectedly cut a series of different interest rates on Tuesday, paving the way for lower key lending rates. The Dow rose by 0.43%, the Nasdaq was up 0.83% while the Russell 2000 Index added 0.69% with the VIX -2.666% lower at 14.61.

Europe

In Europe, equities were also higher boosted by sentiment around US inflation data and action to ease rates in China. The Euro Stoxx 600 Index closed 0.48% higher along with the CAC closed 0.56% higher, the DAX gained 0.82% while the FTSE climbed 0.32%.

In economic data, the United Kingdom’s labour market expectedly tightened in April with 250k jobs added over the three-month period compared to estimates of 150k, while the unemployment rate declined to 3.8% compared to estimates of an increase to 4%. In reaction the Pound strengthened 0.82% to 1.2612 with the 2-year GILT yield up 26 basis points to 4.90%. The data did little to sway rates traders which still see as much as a further 1.375% of tightening by the Bank of England through to February 2024.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

Australia

The ASX is expected to open higher with ASX futures up 44 points or 0.61% to 7,191 after a 0.23% gain on Tuesday. In technology, MP1 rose by 5.23%, WiseTech Global climbed 5.18%, Life360 gained 4.6% and Xero jumped 4.16%. In banking, CBA firmed 0.75%, ANZ 0.35% and WBC 0.25%. In energy, Paladin was the star performer rocketing 9.35% amid expectations of a tightening Uranium market. In materials, BHP was down 0.96%, Rio Tinto lost -1.5%, Newcrest fell 1.4%, and while Fortescue Metals remained flat.

In economic data, the Westpac Consumer Confidence index for June was little changed at 79.2 with economists noting the index has been near recession lows for the past year. The report highlighted that inflation remains a drag on confidence, well ahead of rate hikes and that confidence in the labour market which had been positive is now beginning to turn. New Zealand GDP data is in focus tomorrow, expected to show a -0.1% decline over Q1, which following a -0.6% in Q4 2022 would put the economy in a recession.

Commodities

Oil prices rose on Tuesday after reports from within China to boost the economy, and the US aiming to buy 12 million barrels to replenish strategic reserves. WTI and Brent crude soared 3.43% and 3.24% to $69.42 and $74.17 respectively. In precious metals, the price of spot gold slid -0.72% to $1,943, and the price of spot silver fell by -1.61% to $23.66. Industrial metals were higher with copper rising 2.11% to $383, and SGX Iron Ore up 2.56% at US$111.66. Meanwhile, the price of Bitcoin fell by -0.2% to $25,868.

Economic Calendar

14th June 2023

UK GDP (YoY April) 16:00

IEA Oil Report 18:00

USA PPI (MoM May) 22:30

15th June 2023

USA Fed Interest Rate Decision 04:00

USA Fed Press Conference 04:30

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via [email protected] or by phoning +612 8302 3632.