Global equities once again finished lower on Friday, with the S&P500 officially entering “correction” territory on news that Israeli forces have extended ground activity in Gaza.

United States

Weakness in the S&P500 since the July peak has now seen a decline of 10%, entering what many define as correction territory, the range between a 10-20% decline. While certainly concerning, it is important to note that equity markets spend the bulk of time historically trading between 0-20% from highs rather than constantly making new highs. Factors that have so far contributed to weakness include a rise in longer-term yields, conflict in the Middle East, and despite headline beats in earnings so far for Q3, there has been underlying weakness in results. All of these factors have been headwinds that help explain weakness over the past three months, but do not solely determine where markets go from here, and the recent rise in earnings expectations for the next 12 months as well as robust US GDP are a positive development.

S&P500 Drawdown %

The S&P 500 closed -0.48% lower on Friday, with the majority of the index closing in the red. The Dow Jones fell -1.12%, the Russell 2000 Index dropped -1.21%, while the Nasdaq Composite bucked the trend to rise by 0.38% helped by a 6.83% gain in Amazon.com and 9.29% rise in Intel shares. The yield on the 2-year government bond, which is more sensitive to changes in the interest rate, fell three basis points to 5.00%. The 30-year treasury was up by two basis points to 5.016%, while the 10-year was stable at 4.83%.

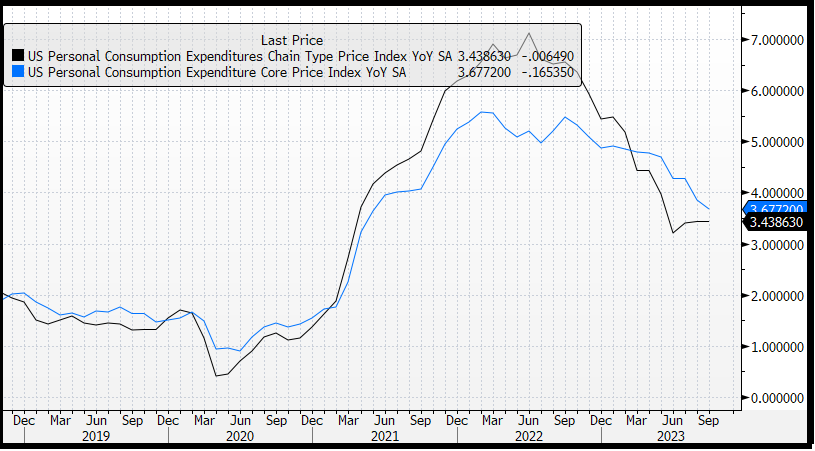

Inflation data on Friday was mostly in line with expectations, with core prices up 0.3% over the month of September and 3.7% over the year. Headline prices rose 3.4% meeting expectations, while slightly ahead of forecasts for the month at 0.4% vs 0.3%. The data did little to sway trader expectations of changes to interest rates when the Federal Reserve meets on Wednesday, with no further hikes priced in. Earnings will remain in focus this week, along with consumer confidence on Tuesday, with non-farm payroll data on Friday rounding off the week.

US PCE Inflation (YoY %)

Europe

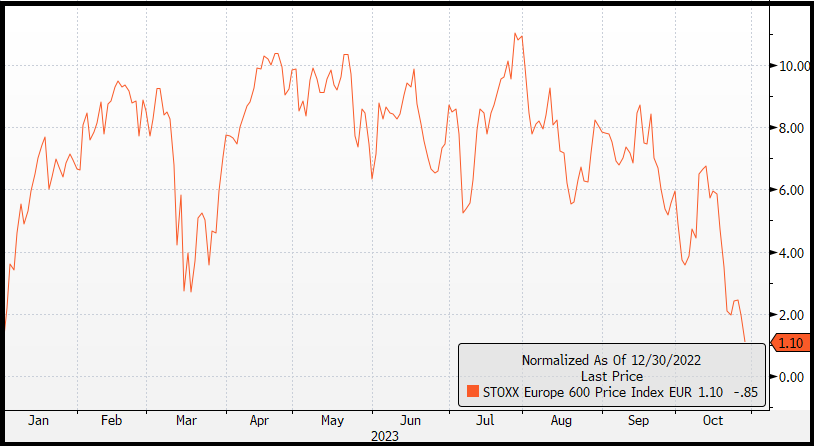

The Euro Stoxx 600 Index fell -0.84% at the end of trading on Friday, now on the verge of turning negative for the year. The DAX was also -0.3% lower along with the CAC -1.36% and FTSE100 -0.86%. For this week, German GDP for Q3 is the main focus tonight, expected to show a -0.3% drop in economic activity over the quarter, and the latest German inflation data, forecast to show a 4% increase in prices over the 12 months. Eurozone inflation for October and Q3 GDP will follow on Tuesday, expected to show the economy was unchanged over the quarter, while core prices are expected to have risen 4.2% over the year. German employment data and a policy decision from the Bank of England are the highlights on Thursday, with Eurozone unemployment released on Friday.

Euro Stoxx 600 YTD %

Australia

The local market is expected to open lower this morning, with ASX200 futures down -67 points or -0.98% to 6,772. The index finished modestly higher by 0.21% on Friday with gains in materials 0.54% and consumer staples 1.33% offsetting weakness in technology -0.8% and industrials -0.64%. Retail sales data for September is due at 11:30 AEDT this morning forecast to show a 0.3% increase over the month. Tuesday will bring the latest housing credit data, along with PMI reports from China and a Bank of Japan policy decision.

Commodities

Oil prices soared on Friday as the conflict between Israel and Hamas saw no signs of a ceasefire. WTI and Brent crude rose by 2.80% and 2.90% to $85.54 and $90.48 respectively. In precious metals, spot gold crossed the two-thousand-dollar mark, rising 1.09% to $2,006.37, while spot silver jumped 1.43% to $23.12. In industrial metals, copper prices climbed by 1.72% to $364.60 while SGX Iron Ore gained 2.24% to $119.67. Meanwhile, the price of bitcoin declined by -1.2% to $33,779.

Economic Calendar

30th October 2023

Australian Retail Sales (MoM Sep) 11:30

German GDP (QoQ Q3) 20:00

Eurozone Consumer Confidence (MoM Oct) 21:00

German Inflation (YoY Oct) 00:00

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via [email protected] or by phoning +612 8302 3632.