US equities finished higher on Friday amid a mixed US employment report, while US markets will be closed on Monday for a public holiday.

United States

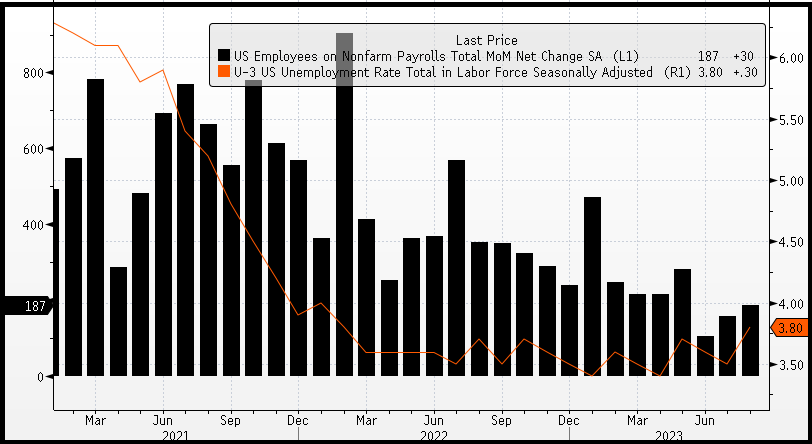

The non-farm payrolls report for August showed employers added 17,000 more jobs compared to forecasts of 170k, bringing the total to 187k. However, this was offset by previous readings being revised lower by 110k over the prior two months, as well as an unexpected increase in the unemployment rate to 3.8% from 3.5% previously. The data points to signs of a cooling labour market and slowing earnings growth with more people returning to the workforce, adding to the case for the Federal Reserve to now leave interest rates on hold. Ahead for the week, investors will be focused on more economic data, notably the ISM Services PMI and Jobless claims report on Thursday.

US Employment (MoM)

The S&P 500 closed 0.18% higher on Friday, with six out of the eleven sectors closing in the green. Energy was the star performer, gaining 2.05% following gains in crude oil, followed by materials up 1.01% and financials adding 0.80%. The Dow Jones climbed 0.33%, the NASDAQ slipped -0.02%, while the Russell 2000 Index rose by 1.11% with the VIX retreating -3.5% to 13.09. US markets will be closed on Monday for a public holiday.

Europe

The Euro Stoxx 600 Index closed marginally lower at the end of trading on Friday, although European equities posted their best week since mid-July. The Euro Stoxx 600 was little changed, down just -0.01% and rose 1.49% for the week. The DAX was -0.67% lower along with the CAC -0.27% while the FTSE100 rose 0.34%. Ahead this week, Eurozone retail sales for July are in focus on Wednesday, followed by the final reading of GDP for Q2 expected to show the Eurozone economy expanded 0.3% over the quarter.

*Note: These prices are based on futures and/or CFD pricing and may therefore differ slightly from spot pricing.

Australia

The ASX 200 Index is expected to open higher this morning, with ASX futures up by 0.43% to 7,274. The Index fell -0.37% on Friday to close at 7,278 with the majority of the index closing in the red. Healthcare was the biggest underperformer, losing -1.42%. PolyNovo plummeted -5.70%, ResMed Inc. shed -2.79% while CSL Ltd dropped -1.62%. Energy stocks rallied with the sector rising 1.58%. Whitehaven Coal jumped 3.94%, Paladin gained 3.55% while Santos and Woodside added 1.83% and 1.57% respectively. In banking, the big names shed value from their share prices namely CBA (-0.81%), WBC (-0.73%), ANZ (-0.63%) and NAB (-0.21%). The materials sectors declined -0.44%. Chalice Mining was the biggest underperformer plummeting -7.28%, Silver Lake Resources fell -3.05%, BHP slipped -0.25%, while RIO climbed 1.18%.

The RBA will hold a policy meeting on Tuesday where the cash rate is forecast to remain unchanged at 4.1% with no further rate increases expected based on futures contracts following last week’s softer-than-expected inflation estimate. On Thursday, RBA Governor Lowe is expected to speak for a final time before his farewell and the transition over to governor-designate Michele Bulock on September 18th. Also in focus on Wednesday is Q2 GDP, expected to show a 0.3% expansion over the quarter and a 1.7% increase in the economy over the 12 months. At the end of the week, Chinese inflation and producer price data will be released, expected to show a 0.1% increase in headline prices over the 12 months to August, with producer prices forecast to decline -3.1% over the same period.

Commodities

In commodities, oil prices soared with WTI and Brent crude rising 2.30% and 1.98% to $85.55 and $88.55 respectively. In precious metals, spot gold fell by -0.01% to $1,940.06 while spot silver declined by -1.04% to $24.19. In industrial metals, the price of copper jumped 1.06% to $381.25 while SGX Iron Ore declined by -0.15% to $113.99.

Economic Calendar

4th September 2023

Swiss GDP (YoY Q2) 17:00

ECB President Lagarde Speech 23:30

This article was written by James Woods, Portfolio Manager, Rivkin Securities Pty Ltd. Enquiries can be made via [email protected] or by phoning +612 8302 3632.