The latest monthly estimate of inflation for October has been released this morning, coming in well below market forecasts.

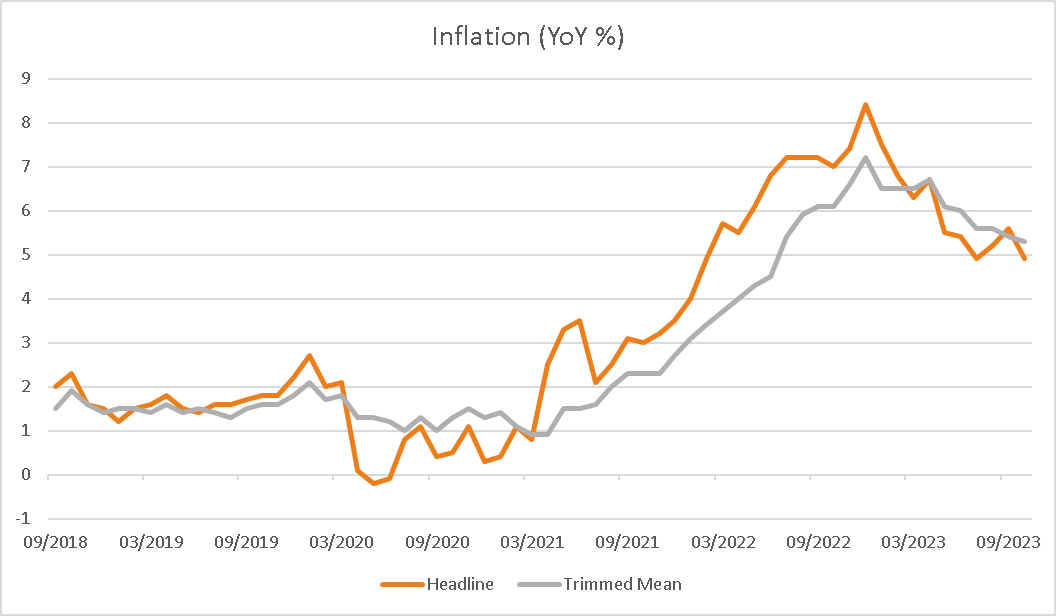

For the 12 months to October, inflation rose 4.9%, well below the consensus estimate of 5.2% and down from 5.6% previously. This is a highly welcome development, especially in the context of recent hawkish comments from RBA Governor Michelle Bullock. Inflation in Australia has lagged global peers both on the way up and down, by roughly six months. Having peaked back in December 2022 at 8.4% inflation continues to trend in the right direction. One potential concern for this is that while headline numbers are moving quickly lower, core measures such as the trimmed mean, declined more modestly from 5.4% to 5.3% and will be a key focus for the RBA.

Somewhat surprisingly, the Australian Dollar is up 0.24% after the data release, although this comes in the context of a weaker USD and lower Treasury yields overnight following more dovish comments from Fed officials. Additionally, the Fed has telegraphed its recent pause and is beginning to more openly discuss the potential for rate cuts, while Australian officials continue to reiterate that some further tightening may be required. This difference is likely to continue being a tailwind for the Australian dollar in the short term.

The market is reacting well, up 0.56% at the time of writing although less than one might expect given the size of the downside miss. Expectations by traders for future policy decisions have eased, with only a 25% chance of a rate increase in the coming months compared to over 50% before the data.

Despite a weaker retail sale reading earlier this week, so far the Australian economy remains fairly resilient with a solid labour market, which coupled with cooling inflation should ease concerns about aggressive monetary policy damaging growth too much, and certainly raises the possibility of a “goldilocks” scenario emerging.

Given comments from RBA officials recently, further tightening cannot be ruled out, although looks significantly less likely now, especially with the effects of the November rate increase yet to flow through into official data. Should we indeed see the RBA join global counterparts on a sustained pause in policy, based on historical precedents this should provide a support backdrop for risk assets, notably equities which have performed strongly after such periods. More analysis on what happens when central banks pause rate hikes can be found here.