United States

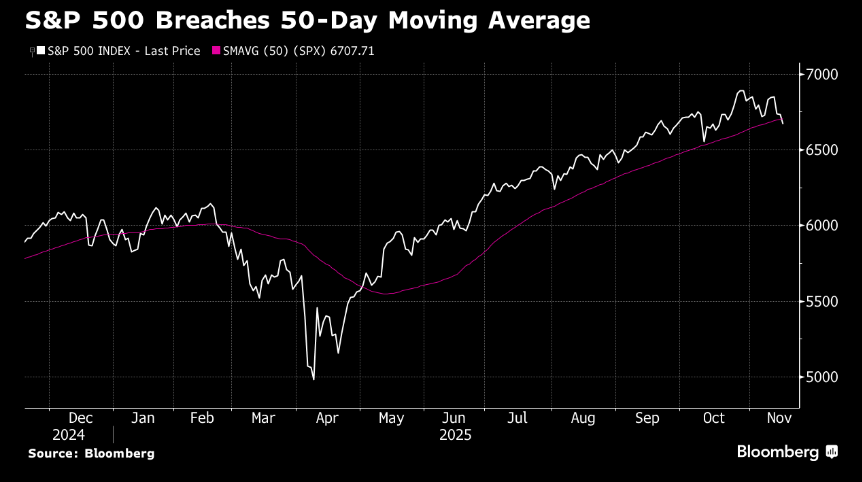

Wall Street’s anxiety intensified overnight as the S&P 500 slid almost 1%. More than 400 stocks in the S&P 500 declined, with the Nasdaq 100 dropping 0.8% and the Dow Jones Industrial Average falling 1.2%. The tech-heavy indices bore the brunt of the selling as investors questioned whether artificial intelligence valuations have run too far ahead of reality.

Nvidia shares slipped 1.8% ahead of Wednesday’s earnings report, which has become the focal point for nervous traders. Options markets are pricing in a potential 6.5% swing in either direction when results are released after Wednesday’s closing bell – the chipmaker’s highest implied move in a year. Adding to the uncertainty, Peter Thiel’s hedge fund Thiel Macro sold its entire stake in Nvidia during the third quarter, marking another high-profile retreat from AI investments.

Not all news was gloomy, however. Alphabet climbed 3.1% after Warren Buffett’s Berkshire Hathaway disclosed it had acquired 17.9 million shares, valued at $4.9 billion, during the third quarter. The investment provided a rare bright spot in an otherwise downbeat session.

Federal Reserve commentary added another layer of complexity to the market mood. Vice Chair Philip Jefferson struck a neutral tone, saying labour market risks have tilted to the downside while inflation risks have eased. More encouragingly for rate cut advocates, Fed Governor Christopher Waller backed a December reduction, stating he would support another quarter-point cut when policymakers meet on 9-10 December. His comments, delivered in a speech titled “The case for continuing rate cuts”, helped trim some losses late in the session.

Despite Waller’s dovish stance, futures markets show investors place less than 50% odds on a December rate cut, down from nearly 100% probability following the September decision. Treasury yields edged two basis points lower to 4.13%, while Bitcoin continued its slide, falling below $92,000.

Europe

European markets extended their losing streak for a third consecutive day, with the Stoxx 600 falling 0.5% as the continent joined Wall Street’s cautious mood. Technology stocks led the retreat, declining 1.2% as semiconductor shares felt additional pressure following tepid guidance from US chip-equipment maker Applied Materials.

Not all sectors struggled, however. Defence stocks outperformed after Saab surged 2.8% on news of a €3.1 billion deal for fighter jets, while Dassault Aviation jumped 4.6% after Ukraine committed to purchasing 100 Rafale jets and 55 locomotives from Alstom.

Energy shares rose 0.7%, closing at a 2008 high as oil prices steadied. Siemens Energy gained 3.4% following a broker upgrade, while TotalEnergies added 0.5% after agreeing to buy a stake in power assets for €5.1 billion.

The standout performer was advertising agency WPP, which soared 11% after reports emerged that French rival Havas had expressed interest in the London-listed firm. The media sector gained ground despite weakness elsewhere.

Banks underperformed, falling 0.9%, with Deutsche Bank dropping 3.3% despite pledging higher returns and payouts in a strategy update. HSBC slipped 1% amid reports that George Osborne is a contender for the chairman role.

Utilities climbed 0.7% to close at a 2008 high, with Italian power giant Enel rising 1.2% to a record closing level. The sector’s advance came as investors sought defensive positioning amid broader market uncertainty.

Automotive shares suffered their biggest daily drop in over a month, declining 1.7%, with Ferrari, Mercedes-Benz, and Stellantis leading losses. Reports that Renault and Nissan are in talks about reviving their alliance failed to lift sentiment in the sector.

Australia

Australian investors face a cautious start to Tuesday, with ASX 200 futures trimming earlier losses to point towards a 0.6% decline after Wall Street extended its losing streak.

The local market closed essentially flat on Monday, with the ASX 200 edging up just 1.9 points to 8,636.40. Energy and property gains offset losses in the financials sector, providing some stability as global volatility picked up.

ALS reported strong results, lifting underlying profit 17.2% to $178.4 million as commodities demand offset softer conditions in life sciences. The company upgraded its full-year organic revenue growth guidance to 6-8%, with the commodities division now expected to grow 12-14%. ALS declared a 19.4¢ interim dividend.

Catapult posted 19% constant-currency growth in annualised contract value to $US115.8 million in the first half of fiscal 2026, driven by gains across its Performance & Health and Tactics & Coaching divisions. Revenue rose 16% to $US67.6 million.

EROAD secured a significant five-year agreement with Cleanaway to deliver vehicle monitoring and compliance systems across the waste group’s 3,000-plus heavy-vehicle fleet. The deal is expected to add more than $5 million in annual recurring revenue.

Fletcher Building confirmed media reports regarding the potential divestment of its Residential Development business, stating it is talking to interested parties as part of a strategic review. However, the company provided no further details.

Morgan Stanley lifted its ASX 200 target to 9,250 for the next 12 months, driven by earnings recovery and elevated valuations. However, the firm is reducing exposure to property and consumer stocks due to doubts over near-term rate cuts.

Looking ahead, the Reserve Bank of Australia will release minutes from its latest policy meeting on Tuesday. Economists expect the minutes to reinforce the view that interest rate cuts remain distant, with inflation pressures still elevated despite some moderation.

Commodities and currencies

Gold fell 1% overnight to $US4,040.26 an ounce as dwindling expectations of a December US rate cut weighed on the precious metal. Despite the near-term headwinds, structural tailwinds such as geopolitical uncertainty, concerns about US debt sustainability, and central bank buying are expected to support investment demand over the medium and long term.

Oil prices steadied, with West Texas Intermediate crude edging down 0.5% to $US59.76 a barrel. Brent crude last traded around $US64.06 a barrel as signs of resumed activity at a key Russian port were balanced against wider geopolitical risks, including Ukraine’s recent attacks on Russian energy infrastructure and Iran’s seizure of a tanker near the Strait of Hormuz.

Iron ore provided some positive news, rising 1.6% to $US104.25 a tonne, offering support for Australian resource stocks.

The Australian dollar weakened 0.8% to US64.85¢ as broader risk aversion and a stronger US dollar weighed on the currency. The greenback gained ground across most major pairs as investors sought safety ahead of this week’s key data releases.

Bitcoin’s rout deepened, with the cryptocurrency falling 3% to $US91,533 as the digital asset extended its retreat from October’s record highs above $US126,000. The decline reflects broader risk-off sentiment and follows nearly $900 million in outflows from Bitcoin investment funds.

Economic Calendar

US:

- Factory Orders Aug 02:00

- Durable Goods Orders Aug 02:00

This article was written by Calvin Curdie, Rivkin Securities Pty Ltd. Enquiries can be made via [email protected] or by phoning +612 8302 3632.