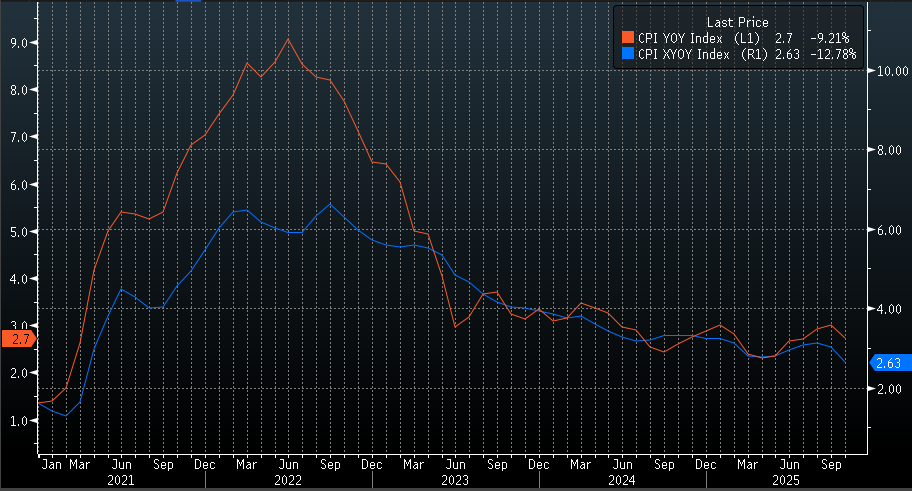

United States

US markets found fresh footing overnight after a softer-than-expected inflation print triggered a relief rally across equities and bonds. Data showing consumer price pressures eased sharply in November, marking the slowest annual pace since early 2021, encouraged investors who have been wary that sticky inflation could delay further monetary easing. While the report was clouded by distortions linked to the US government shutdown, markets largely welcomed the signal that price pressures are directionally cooling. US inflation surprised to the downside, with both headline and core readings coming in below expectations of 3.1% and 3.0% respectively with actuals of 2.7% and 2.6%, reinforcing the view that price pressures are continuing to ease.

The S&P 500 rose 0.7%, snapping a four-day losing streak, while the Nasdaq 100 gained 1.3% as technology stocks led the rebound. Megacap shares outperformed, with Micron Technology surging 11% after issuing an upbeat outlook that reinforced confidence in sustained demand for artificial intelligence-related hardware. The Dow Jones Industrial Average was little changed, reflecting more cautious moves in cyclicals.

Bond markets also reacted swiftly. The yield on the 10-year US Treasury fell four basis points to 4.12%, while two-year yields slipped to 3.46%, as traders modestly lifted expectations for rate cuts in 2026. Interest-rate swaps now imply roughly a 22% chance of a cut at the Federal Reserve’s January meeting, with two reductions still priced in for next year. The US dollar was largely unchanged, signalling a measured response rather than a full-scale repricing of policy expectations.

Core inflation, excluding food and energy, rose 2.6% from a year earlier. Despite questions around data quality due to the shutdown affecting October collection, the report reinforced the Federal Reserve’s recent wait-and-see stance. Scrutiny is now likely to intensify ahead of the December CPI release, which markets see as a more reliable gauge.

Europe

European equities closed at record highs, extending a strong run as global investors responded positively to the US inflation surprise. The Stoxx Europe 600 advanced 1% to finish at its highest ever close, tracking a sixth consecutive month of gains, the longest winning streak since 2021. Gains were broad-based, though sentiment remained attentive to valuation concerns around artificial intelligence-linked stocks.

Central bank decisions added complexity to the regional backdrop. The European Central Bank left interest rates unchanged for a fourth straight meeting and signalled confidence in firmer economic growth, with inflation forecast to return to its 2% target in 2028. In contrast, the Bank of England lowered its benchmark rate to 3.75%, the lowest level in almost three years, reflecting easing domestic inflation pressures. UK government bonds underperformed US Treasuries following the decision, while Britain’s FTSE 100 ended 0.6% higher after a choppy session.

At the stock level, Whitbread surged 6.3% after calls from an activist investor for a strategic review, while Aeroports de Paris fell sharply after regulators rejected proposed fee increases. European retail stocks outperformed, supported by optimism around large apparel names.

Australia

The Australian sharemarket edged higher, snapping a three-day losing streak, though gains were modest and uneven. The S&P/ASX 200 added three points to close at 8,588.2, with just seven of the 11 sectors finishing in positive territory. Technology stocks staged a late rebound, helping the index claw back earlier losses, while energy and uranium stocks weighed on sentiment.

Local technology names had a mixed session. WiseTech Global rose 1.6% and Xero gained 2.5%, but NextDC slid 4.4% and Megaport fell 1.8%. Life360 continued its recent slide, closing at a six-month low after a steep pullback from July highs.

Energy stocks underperformed despite firmer oil prices. Woodside Energy dropped 2.7% after announcing its chief executive would depart to take the top role at BP. Santos bucked the trend, rising 1%, supported by higher crude prices and favourable legal news. Uranium stocks were heavily sold, led by a 25% plunge in Boss Energy following a downgrade to its Honeymoon project.

In corporate news, Bapcor jumped 15.5% after the resignation of its chief executive, while Bendigo Bank fell 1.5% amid news of an AUSTRAC investigation into compliance processes. APA Group edged higher after agreeing to sell its stake in the Allgas gas distribution network.

Looking ahead, futures point to a stronger open, with the ASX 200 expected to rise around 0.6%, taking cues from Wall Street’s rebound.

Commodities and currencies

Commodity markets were relatively subdued overnight. West Texas Intermediate crude rose marginally to US56.01 a barrel, while Brent crude traded firmer near US59.79. Spot gold eased 0.3% to around US4,323 an ounce, reflecting a steadier US dollar and lower bond yields.

In currency markets, the Australian dollar strengthened 0.2% to trade near US66.17 cents. The euro slipped slightly to US1.1724, while the British pound was little changed at US1.3385. The Japanese yen firmed modestly against the dollar.

Cryptocurrencies moved lower, with Bitcoin falling around 1.6% to near US84,600 and Ether down 1.2%.

Economic Calendar

No major data releases

This article was written by Calvin Curdie, Rivkin Securities Pty Ltd. Enquiries can be made via [email protected] or by phoning +612 8302 3632.