Apple Inc. designs, manufactures, and markets smartphones, personal computers, tablets, wearables, and accessories worldwide.

Apple’s latest update paints a mixed but strategically significant picture as the company navigates softer iPhone demand in China, escalating tariff pressures, and a renewed push into artificial intelligence. Despite uneven product growth, the technology giant remains anchored by its expanding services division, which continues to underpin margins and long-term profitability.

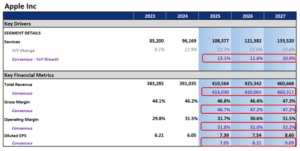

Apple reported quarterly revenue of approximately USD 102 billion, up 7.9 percent year on year and outpacing the prior period’s 6.1 percent growth. Services were the standout performer, climbing 15 percent and beating consensus estimates by over two percentage points. The division now represents about 26 percent of total sales and delivers roughly twice the profitability of hardware products. Mac sales rose 12.7 percent to USD 8.7 billion, while iPad revenue was flat. Meanwhile, sales of wearables, home and accessories declined, highlighting Apple’s reliance on its high-margin digital ecosystem for growth.

Figure 1: Key financial Metrics (Source: Bloomberg)

This performance reinforces a long-term trend. Over the past three years, Apple’s gross margin has expanded by 350 basis points to 46.7 percent, largely due to the growing share of services. With continued double-digit expansion expected into early FY26, the segment remains Apple’s most stable engine for revenue and margin growth.

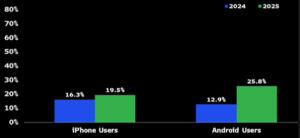

Artificial intelligence is becoming central to Apple’s next phase. While the company has lagged Android rivals in rolling out on-device AI features, management’s plans for a revamped Siri (powered by third-party AI models) could spark a faster upgrade cycle. Surveys show only around 52 percent of iPhone users intend to upgrade in the next 12 months, compared with 64 percent of Android users, underscoring the importance of Apple’s upcoming AI integrations.

Figure 2: Consumer Intent to Upgrade (Source: Bloomberg Study)

The expected 10–12 percent rise in iPhone sales during fiscal 1Q26, compared with market expectations of 6 percent, should help ease investor concerns following weak results in Greater China. Supply shortages, rather than structural demand loss, appear to have driven the regional weakness. Upcoming iPhone models and potential price increases could further support revenue despite modest unit growth.

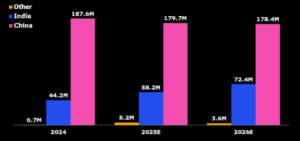

Trade tensions continue to loom large. Proposed US tariffs on Chinese imports could increase Apple’s quarterly costs by about USD 1.9 billion, with accessories most affected. Each 10 percent rise in import tariffs would compress operating margins by roughly 140 basis points. Apple’s accelerated move to assemble iPhones in India, expected to reach 30 percent of production by 2026, may mitigate some exposure, though it risks straining relations with China and alienating local consumers.

Figure 3: iPhone Production by Country (source: Counterpoint)

While the strategy diversifies risk, China remains critical. The market accounts for 17 percent of revenue and nearly a quarter of Apple’s global installed iPhone base. Any consumer backlash or regulatory pushback could have a pronounced effect on overall performance.

Apple also faces ongoing antitrust scrutiny over its App Store model. Following a court ruling in the Epic Games case, the company could see a USD 1 billion reduction in revenue, and a 5 cent hit to earnings per share, for every 10 percent of transactions that move outside its ecosystem. Although Apple may lower fees or adjust pricing for other services to offset losses, this remains a medium-term profitability risk.

Looking ahead, Apple’s path will likely be defined by its ability to sustain services growth while re-energising its product cycle through AI innovation. The company’s disciplined capital management, evident in USD 20 billion in quarterly buybacks, supports shareholder returns even amid external volatility. Yet, heavy dependence on China for both sales and supply chain resilience remains the key vulnerability. If Apple can successfully navigate geopolitical pressures and accelerate AI-driven upgrades, it may reclaim stronger momentum heading into fiscal 2026.