United States

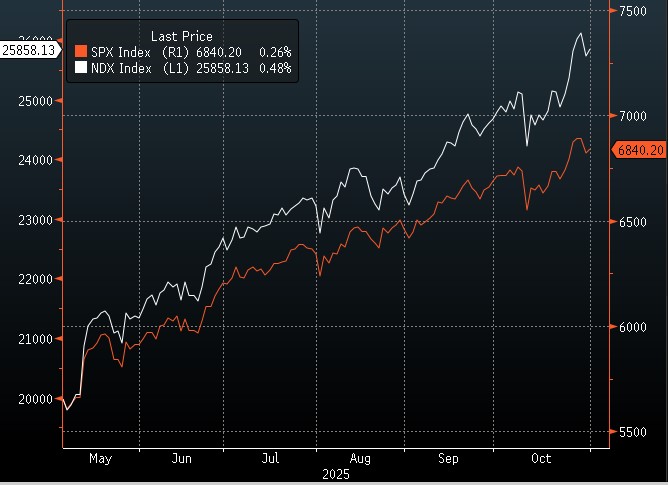

Wall Street extended its historic rally on Friday as optimism around corporate earnings outweighed concerns over valuations and the concentration of gains in major technology stocks. The S&P 500 rose 0.3% to about 6,840, marking its sixth consecutive monthly advance, the longest streak since 2021. The Nasdaq 100 gained 0.5%, driven by strength in the so-called “Magnificent Seven” tech giants, which climbed 1.2% overall. Amazon jumped nearly 10% on strong cloud growth, while Apple’s share price eased after a sales decline in China tempered enthusiasm ahead of the holiday season.

Investor sentiment remained buoyant despite lingering concerns about market breadth and high valuations. Since the April sell-off, the S&P 500 has surged almost 40%, supported by expectations that US rate cuts will sustain corporate profitability. Approximately 60% of S&P 500 companies have now reported results, with most surpassing forecasts.

In fixed income, Treasury yields were largely unchanged after the Federal Reserve signalled no imminent rate cuts, keeping the 10-year yield near 4.09%. The US dollar strengthened, recording its best month since July.

Corporate highlights included upbeat results from Cloudflare, Coinbase, and Colgate-Palmolive, while Exxon Mobil and Chevron pursued divergent strategies amid expectations of a crude supply glut. Oil prices edged up 0.6% to USD 60.91 a barrel, and spot gold slipped 0.6% to USD 3,998.88 an ounce.

Nasdaq100 vs SP500, showing outperformance of the Mag 7 and Tech

Europe

European equities edged lower, with the Stoxx 600 falling 0.1% amid a wave of earnings announcements and an unchanged European Central Bank policy stance. Automakers led the declines as Stellantis plunged 8.6% after warning of one-off charges, dragging the automotive sector 1.4% lower. Mercedes-Benz and Volkswagen also slipped following earnings updates.

Energy shares provided some offset, rising 0.2% after solid results from BP and Shell. Utility stocks also outperformed, with Enel and Fortum among the top gainers. Technology names rose 0.9%, lifted by ASML and ASM International, while media and telecoms underperformed, weighed by WPP and Deutsche Telekom.

Elsewhere, Campari rallied 11% on a profit surprise despite weaker Aperol sales, while Schneider Electric and Technip Energies slid after disappointing quarterly numbers. Banks were mixed as ING gained 5.7% on strong results, while SocGen fell 3.6% due to a tax hit.

Overall, sector rotation remained in focus, with investors reacting to uneven earnings momentum and cautious forward guidance across industries.

Australia

Australian shares were steady on Friday, with the S&P/ASX 200 closing almost unchanged at 8,881.90. Gains in energy and gold stocks were offset by weakness in consumer-goods names.

Vault Minerals rose 5.8%, leading the day’s advancers, while Westgold and Regis Resources also climbed over 5% as bullion prices remained elevated. Among the decliners, Steadfast fell 9.7% following earnings updates, and Lovisa dropped 4.8%, its largest fall in four months.

Investors are now turning their attention to Westpac’s full-year results, with the bank expected to report a net profit of around AUD 6.9 billion, down 1% from the previous year. The update will provide a key read on margin pressures and loan growth across Australia’s major lenders.

The latest inflation data continues to shape rate expectations ahead of the Reserve Bank of Australia’s meeting on Tuesday. Markets have priced out the chance of a Melbourne Cup Day rate cut after stronger-than-expected CPI figures suggested that price pressures remain persistent. The cash rate is widely expected to stay at 3.6%, with the RBA likely to revise inflation forecasts higher in its upcoming Statement on Monetary Policy.

Commodities and currencies

Commodity markets were mixed overnight. Brent and WTI crude extended modest gains after the US ruled out fresh military action in Venezuela, while gold prices eased from record highs near USD 4,000 per ounce.

In currency markets, the Bloomberg Dollar Spot Index rose 0.2%, supported by higher US yields. The euro fell 0.3% to USD 1.1528, and the yen hovered near 154.1 per dollar. Bitcoin gained 2% to USD 109,660, while ether advanced 3.4% to USD 3,885.

With US equities entering what is historically their strongest two-month period of the year, investors are watching whether the rally can broaden beyond mega-cap tech. Locally, the ASX is poised to open slightly lower as traders digest Wall Street’s mixed session and await the RBA’s policy guidance.

Economic Calendar

US:

- ISM Manufacturing (Oct) 02:00

- Construction Spending (Sep) 02:00

AU:

- Building Approvals (Sep) 11:30

EU:

- HCOB Eurozone Manufacturing PMI (Oct) 20:00

This article was written by James Woods, Rivkin Securities Pty Ltd. Enquiries can be made via [email protected] or by phoning +612 8302 3632.